Revised Acts

This Act

Download PDFs

On the eISB

Consumer Credit Act 1995

FIRST SCHEDULE

Council Directive 87/102/EEC and Council Directive 90/88/EEC

Part I

COUNCIL DIRECTIVE

of 22 December 1986

for the approximation of the laws, regulations and administrative provisions of the Member States concerning consumer credit

(87/102/EEC)

THE COUNCIL OF THE EUROPEAN COMMUNITIES,

Having regard to the Treaty establishing the European Economic Community, and in particular Article 100 thereof,

Having regard to the proposal from the Commission(1),

Having regard to the opinion of the European Parliament(2),

Having regard to the opinion of the Economic and Social Committee(3),

Whereas wide differences exist in the laws of the Member States in the field of consumer credit;

Whereas these differences of law can lead to distortions of competition between grantors of credit in the common market;

Whereas these differences limit the opportunities the consumer has to obtain credit in other Member States; whereas they affect the volume and the nature of the credit sought, and also the purchase of goods and services;

Whereas, as a result, these differences have an influence on the free movement of goods and services obtainable by consumers on credit and thus directly affect the functioning of the common market;

Whereas, given the increasing volume of credit granted in the Community to consumers, the establishment of a common market in consumer credit would benefit alike consumers, grantors of credit, manufacturers, wholesalers and retailers of goods and providers of services;

Whereas the programmes of the Europen Economic Community for a consumer protection and information policy(4) provide, inter alia, that the consumer should be protected against unfair credit terms and that a harmonization of the general conditions governing consumer credit should be undertaken as a priority;

Whereas differences of law and practice result in unequal consumer protection in the field of consumer credit from one Member State to another;

Whereas there has been much change in recent years in the types of credit available to and used by consumers; whereas new forms of consumer credit have emerged and continue to develop;

Whereas the consumer should receive adequate information on the conditions and cost of credit and on his obligations; whereas this information should include, inter alia, the annual percentage rate of charge for credit, or, failing that, the total amount that the consumer must pay for credit; whereas, pending a decision on a Community method or methods of calculating the annual percentage rate of charge, Member States should be able to retain existing methods or practices for calculating this rate, or failing that, should establish provisions for indicating the total cost of the credit to the consumer;

Whereas the terms of credit may be disadvantageous to the consumer; whereas better protection of consumers can be achieved by adopting certain requirements which are to apply to all forms of credit;

Whereas, having regard to the character of certain credit agreements or types of transaction, these agreements or transactions should be partially or entirely excluded from the field of application of this Directive;

Whereas it should be possible for Member States, in consultation with the Commission, to exempt from the Directive certain forms of credit of a non-commercial character granted under particular conditions;

Whereas the practices existing in some Member States in respect of authentic acts drawn up before a notary or judge are such as to render the application of certain provisions of this Directive unnecessary in the case of such acts; whereas it should therefore be possible for Member States to exempt such acts from those provisions;

Whereas credit agreements for very large financial amounts tend to differ from the usual consumer credit agreements; whereas the application of the provisions of this Directive to agreements for very small amounts could create unnecessary administrative burdens both for consumers and grantors of credit; whereas therefore, agreements above or below specified financial limits should be excluded from the Directive;

Whereas the provision of information on the cost of credit in advertising and at the business premises of the creditor or credit broker can make it easier for the consumer to compare different offers;

Whereas consumer protection is further improved if credit agreements are made in writing and contain certain minimum particulars concerning the contractual terms;

Whereas, in the case of credit granted for the acquisition of goods, Member States should lay down the conditions in which goods may be repossessed, particularly if the consumer has not given his consent; whereas the account between the parties should upon repossession be made up in such manner as to ensure that the repossession does not entail any unjustified enrichment;

Whereas the consumer should be allowed to discharge his obligations before the due date; whereas the consumer should then be entitled to an equitable reduction in the total cost of the credit;

Whereas the assignment of the creditor's rights arising under a credit agreement should not be allowed to weaken the position of the consumer;

Whereas those Member States which permit consumers to use bills of exchange, promissory notes or cheques in connection with credit agreements should ensure that the consumer is suitably protected when so using such instruments;

Whereas, as regards goods or services which the consumer has contracted to acquire on credit, the consumer should, at least in the circumstances defined below, have rights vis-à-vis the grantor of credit which are in addition to his normal contractual rights against him and against the supplier of the goods or services; whereas the circumstances referred to above are those where grantor of credit and the supplier of goods or services have a pre-existing agreement whereunder credit is made available exclusively by that grantor of credit to customers of that supplier for the purpose of enabling the consumer to acquire goods or services from the latter;

Whereas the ECU is as defined in Council Regulation (EEC) No 3180/78(1), as last amended by Regulation (EEC) No 2626/84(2); whereas Member States should to a limited extent be at liberty to round off the amounts in national currency resulting from the conversion of amounts of this Directive expressed in ECU; whereas the amounts in this Directive should be periodically re-examined in the light of economic and monetary trends in the Community, and, if need be, revised;

Whereas suitable measures should be adopted by Member States for authorising persons offering credit or offering to arrange credit agreements or for inspecting or monitoring the activities of persons granting credit or arranging for credit to be granted or for enabling consumers to complain about credit agreements or credit conditions;

Whereas credit agreements should not derogate, to the detriment of the consumer, from the provisions adopted in implementation of this Directive or corresponding to its provisions; whereas those provisions should not be circumvented as a result of the way in which agreements are formulated;

Whereas, since this Directive provides for a certain degree of approximation of the laws, regulations and administrative provisions of the Member States concerning consumer credit and for a certain level of consumer protection, Member States should not be prevented from retaining or adopting more stringent measures to protect the consumer, with due regard for their obligations under the Treaty;

Whereas, not later than 1 January 1995, the Commission should present to the Council a report concerning the operation of this Directive,

HAS ADOPTED THIS DIRECTIVE:

Article 1

1. This Directive applies to credit agreements.

2. For the purpose of this Directive:

(a) ‘consumer’ means a natural person who, in transactions covered by this Directive, is acting for purposes which can be regarded as outside his trade or profession;

(b) ‘creditor’ means a natural or legal person who grants credit in the course of his trade, business or profession, or a group of such persons;

(c) ‘credit agreement’ means an agreement whereby a creditor grants or promises to grant to a consumer a credit in the form of a deferred payment, a loan or other similar financial accommodation.

Agreements for the provision on a continuing basis of a service or a utility, where the consumer has the right to pay for them, for the duration of their provision, by means of instalments, are not deemed to be credit agreements for the purpose of this Directive;

(d) ‘total cost of the credit to the consumer’ means all the costs of the credit including interest and other charges directly connected with the credit agreement, determined in accordance with the provisions or practices existing in, or to be established by, the Member States.

(e) ‘annual percentage rate of charge’ means the total cost of the credit to the consumer expressed as an annual percentage of the amount of the credit granted and calculated according to existing methods of the Member States.

Article 2

1. This Directive shall not apply to:

(a) credit agreements or agreements promising to grant credit:

—intended primarily for the purpose of acquiring or retaining property rights in land or in an existing or projected building,

—intended for the purpose of renovating or improving a building as such;

(b) hiring agreements except where these provide that the title will pass ultimately to the hirer;

(c) credit granted or made available without payment of interest or any other charge;

(d) credit agreements under which no interest is charged provided the consumer agrees to repay the credit in a single payment;

(e) credit in the form of advances on a current account granted by a credit institution or financial institution other than on credit card accounts.

Nevertheless, the provisions of Article 6 shall apply to such credits;

(f) credit agreements involving amounts less than 200 ECU or more than 20 000 ECU;

(g) credit agreements under which the consumer is required to repay the credit:

—either, within a period not exceeding three months,

—or, by a maximum number of four payments within a period not exceeding 12 months.

2. A Member State may, in consultation with the Commission, exempt from the application of this Directive certain types of credit which fulfil the following conditions:

—they are granted at rates of charge below those prevailing in the market, and

—they are not offered to the public generally.

3. The provisions of Article 4 and of Articles 6 to 12 shall not apply to credit agreements or agreements promising to grant credit, secured by mortgage on immovable property, in so far as these are not already excluded from the Directive under paragraph 1 (a) of this Article.

4. Member States may exempt from the provisions of Articles 6 to 12 credit agreements in the form of an authentic act signed before a notary or judge.

Article 3

Without prejudice to Council Directive 84/450/EEC of 10 September 1984 relating to the approximation of the laws, regulations and administrative provisions of the Member States concerning misleading advertising(1), and to the rules and principles applicable to unfair advertising, any advertisement, or any offer which is displayed at business premises, in which a person offers credit or offers to arrange a credit agreement and in which a rate of interest or any figures relating to the cost of the credit are indicated, shall also include a statement of the annual percentage rate of charge, by means of a representative example if no other means is practicable.

Article 4

1. Credit agreements shall be made in writing. The consumer shall receive a copy of the written agreement.

2. The written agreement shall include:

(a) a statement of the annual percentage rate of charge;

(b) a statement of the conditions under which the annual percentage rate of charge may be amended.

In cases where it is not possible to state the annual percentage rate of charge, the consumer shall be provided with adequate information in the written agreement. This information shall at least include the information provided for in the second indent of Article 6 (1).

3. The written agreement shall further include the other essential terms of the contract.

By way of illustration, the Annex to this Directive contains a list of terms which Member States may require to be included in the written agreement as being essential.

Article 5

By way of derogation from Articles 3 and 4 (2), and pending a decision on the introduction of a Community method or methods of calculating the annual percentage rate of charge, those Member States which, at the time of notification of this Directive, do not require the annual percentage rate of charge to be shown or which do not have an established method for its calculation, shall at least require the total cost of the credit to the consumer to be indicated.

Article 6

1. Notwithstanding the exclusion provided for in Article 2 (1) (e), where there is an agreement between a credit institution or financial institution and a consumer for the granting of credit in the form of an advance on a current account, other than on credit card accounts, the consumer shall be informed at the time or before the agreement is concluded:

—of the credit limit, if any,

—of the annual rate of interest and the charges applicable from the time the agreement is concluded and the conditions under which these may be amended,

—of the procedure for terminating the agreement.

This information shall be confirmed in writing.

2. Furthermore, during the period of the agreement, the consumer shall be informed of any change in the annual rate of interest or in the relevant charges at the time it occurs. Such information may be given in a statement of account or in any other manner acceptable to Member States.

3. In Member States where tacitly accepted overdrafts are permissible, the Member States concerned shall ensure that the consumer is informed of the annual rate of interest and the charges applicable, and of any amendment thereof, where the overdraft extends beyond a period of three months.

Article 7

In the case of credit granted for the acquisition of goods, Member States shall lay down the conditions under which goods may be repossessed, in particular if the consumer has not given his consent. They shall further ensure that where the creditor recovers possession of the goods the account between the parties shall be made up so as to ensure that the repossession does not entail any unjustified enrichment.

Article 8

The consumer shall be entitled to discharge his obligations under a credit agreement before the time fixed by the agreement. In this event, in accordance with the rules laid down by the Member States, the consumer shall be entitled to an equitable reduction in the total cost of the credit.

Article 9

Where the creditor's rights under a credit agreement are assigned to a third person, the consumer shall be entitled to plead against that third person any defence which was available to him against the original creditor, including set-off where the latter is permitted in the Member State concerned.

Article 10

The Member States which, in connection with credit agreements, permit the consumer:

(a) to make payment by means of bills of exchange including promissory notes;

(b) to give security by means of bills of exchange including promissory notes and cheques,

shall ensure that the consumer is suitably protected when using these instruments in those ways.

Article 11

1. Member States shall ensure that the existence of a credit agreement shall not in any way affect the rights of the consumer against the supplier of goods or services purchased by means of such an agreement in cases where the goods or services are not supplied or are otherwise not in conformity with the contract for their supply.

2. Where:

(a) in order to buy goods or obtain services the consumer enters into a credit agreement with a person other than the supplier of them;

and

(b) the grantor of the credit and the supplier of the goods or services have a pre-existing agreement whereunder credit is made available exclusively by that grantor of credit to customers of that supplier for the acquisition of goods or services from that supplier; and

(c) the consumer referred to in subparagraph (a) obtains his credit pursuant to that pre-existing agreement; and

(d) the goods or services covered by the credit agreement are not supplied, or are supplied only in part, or are not in conformity with the contract for supply of them; and

(e) the consumer has pursued his remedies against the supplier but has failed to obtain the satisfaction to which he is entitled,

the consumer shall have the right to pursue remedies against the grantor of credit. Member States shall determine to what extent and under what conditions these remedies shall be exercisable.

3. Paragraph 2 shall not apply where the individual transaction in question is for an amount less than the equivalent of 200 ECU.

Article 12

1. Member States shall:

(a) ensure that persons offering credit or offering to arrange credit agreements shall obtain official authorization to do so, either specifically or as suppliers of goods and services; or

(b) ensure that persons granting credit or arranging for credit to be granted shall be subject to inspection or monitoring of their activities by an institution or official body; or

(c) promote the establishment of appropriate bodies to receive complaints concerning credit agreements or credit conditions and to provide relevant information or advice to consumers regarding them.

2. Member States may provide that the authorization referred to in paragraph 1 (a) shall not be required where persons offering to conclude or arrange credit agreements satisfy the definition in Article 1 of the first Council Directive of 12 December 1977 on the co-ordination of laws, regulations and administrative provisions relating to the taking up and pursuit of the business of credit institutions(1) and are authorized in accordance with the provisions of that Directive.

Where persons granting credit or arranging for credit to be granted have been authorized both specifically, under the provisions of paragraph 1 (a) and also under the provisions of the aforementioned Directive, but the latter authorization is subsequently withdrawn, the competent authority responsible for issuing the specific authorization to grant credit under paragraph 1 (a) shall be informed and shall decide whether the person concerned may continue to grant credit, or arrange for credit to be granted, or whether the specific authorization granted under paragraph 1 (a) should be withdrawn.

Article 13

1. For the purposes of this Directive, the ECU shall be that defined by Regulation (EEC) No 3180/78, as amended by Regulation (EEC) No 2626/84. The equivalent in national currency shall initially be calculated at the rate obtaining on the date of adoption of this Directive.

Member States may round off the amounts in national currency resulting from the conversion of the amounts in ECU provided such rounding off does not exceed 10 ECU.

2. Every five years, and for the first time in 1995, the Council, acting on a proposal from the Commission, shall examine and, if need be, revise the amounts in this Directive in the light of economic and monetary trends in the Community.

Article 14

1. Member States shall ensure that credit agreements shall not derogate, to the detriment of the consumer, from the provisions of national law implementing or corresponding to this Directive.

2. Member States shall further ensure that the provisions which they adopt in implementation of this directive are not circumvented as a result of the way in which agreements are formulated, in particular by the device of distributing the amount of credit over several agreements.

Article 15

This Directive shall not preclude Member States from retaining or adopting more stringent provisions to protect consumers consistent with their obligations under the Treaty.

Article 16

1. Member States shall bring into force the measures necessary to comply with this Directive not later than 1 January 1990 and shall forthwith inform the Commission thereof.

2. Member States shall communicate to the Commission the texts of the main provisions of national law which they adopt in the field covered by this Directive.

Article 17

Not later than 1 January 1995 the Commission shall present a report to the Council concerning the operation of this Directive.

Article 18

This Directive is addressed to the Member States.

Done at Brussels, 22 December, 1986.

For the Council

The President

G. SHAW.

ANNEX

List of Terms Referred to in Article 4 (3)

1. Credit agreements for financing the supply of particular goods or services:

(i) a description of the goods or services covered by the agreement;

(ii) the cash price and the price payable under the credit agreement;

(iii) the amount of the deposit, if any, the number and amount of instalments and the dates on which they fall due, or the method of ascertaining any of the same if unknown at the time the agreement is concluded;

(iv) an indication that the consumer will be entitled, as provided in Article 8, to a reduction if he repays early;

(v) who owns the goods (if ownership does not pass immediately to the consumer) and the terms on which the consumer becomes the owner of them;

(vi) a description of the security required, if any;

(vii) the cooling-off period, if any;

(viii) an indication of the insurance(s) required, if any, and, when the choice of insurer is not left to the consumer, an indication of the cost thereof.

2. Credit agreements operated by credit cards:

(i) the amount of the credit limit, if any;

(ii) the terms of repayment or the means of determining them;

(iii) the cooling-off period, if any.

3.Credit agreements operated by running account which are not otherwise covered by the Directive:

(i) the amount of the credit limit, if any, or the method of determing it;

(ii) the terms of use and repayment;

(iii) the cooling-off period, if any.

4. Other credit agreements covered by the Directive:

(i) the amount of the credit limit, if any;

(ii) an indication of the security required, if any;

(iii) the terms of repayment;

(iv) the cooling-off period, if any;

(v) an indication that the consumer will be entitled, as provided in Article 8, to a reduction if he repays early.

Part II

COUNCIL DIRECTIVE

of 22 February 1990

amending Directive 87/102/EEC for the approximation of the laws, regulations and administrative provisions of the Member States concerning consumer credit

(90/88/EEC)

THE COUNCIL OF THE EUROPEAN COMMUNITIES,

Having regard to the Treaty establishing the European Economic Community, and in particular Article 100a thereof,

Having regard to the proposal from the Commission(1),

In cooperation with the European Parliament(2),

Having regard to the opinion of the Economic and Social Committee(3),

Whereas Article 5 of Council Directive 87/102/EEC(4) provides for the introduction of a Community method or methods of calculating the annual percentage rate of lcharge for consumer credit;

Whereas it is desirable, in order to promote the establishment and functioning the internal market and to ensure that consumers benefit from a high level of protection, that one method of calculating the said annual percentage rate of charge should be used throughout the Community;

Whereas it is desirable, with a view to introducing such a method and in accordance with the definition of the total cost of credit to the consumer, to draw up a single mathematical formula for calculating the annual percentage rate of charge and for determining credit cost items to be used in the calculation by indicating those costs which must not be taken into account;

Whereas, during a trasitional period, Member States which prior to the date of notification of this Directive, apply laws which permit the use of another mathematical formula for calculating the annual percentage rate of charge may continue to apply such laws;

Whereas, before expiry of the transitional period and in the light of experience, the Council will, on the basis of a proposal from the Commission, take a decision which will make it possible to apply a single Community mathematical formula;

Whereas it is desirable, whenever necessary, to adopt certain hypotheses for calculating the annual percentage rate of charge;

Whereas by virtue of the special nature of loans guaranteed by a mortgage secured on immoveable property it is desirable that such credit should continue to be partially excluded from this Directive;

Whereas the information which must be communicated to the consumer in the written contract should be amplified,

HAS ADOPTED THIS DIRECTIVE:

Article 1

Directive 87/102/EEC is hereby amended as follows:

1. In Article 1 (2), points (d) and (e) shall be replaced by the following:

‘(d) “total cost of the credit to the consumer” means all the costs, including interest and other charges, which the consumer has to pay for the credit.’;

‘(e) “annual percentage rate of charge” means the total cost of the credit to the consumer, expressed as an annual percentage of the amount of the credit granted and calculated in accordance with Article 1a’.

2. The following Article shall be inserted:

‘Article 1a

1. (a) The annual percentage rate of charge, which shall be that equivalent, on an annual basis, to the present value of all commitments (loans, repayments and charges), future or existing, agreed by the creditor and the borrower, shall be calculated in accordance with the mathematical formula set out in Annex II.

(b) Four examples of the method of calculation are given in Annex III, by way of illustration.

2. For the purpose of calculating the annual percentage rate of charge, the “total cost of the credit to the consumer” as defined in Article 1 (2) (d) shall be determined, with the exception of the following charges:

(i) charges payable by the borrower for non-compliance with any of his commitments laid down in the credit agreement;

(ii) charges other than the purchase price which, in purchases of goods or services, the consumer is obliged to pay whether the transactions is paid in cash or by credit;

(iii) charges for the transfer of funds and charges for keeping an account intended to receive payments towards the reimbursement of the credit the payment of interest and other charges except where the consumer doesn ot have reasonable freedom of choice in the matter and where such charges are abnormally high; this provision shall not, however, apply to charges for collection of such reimbursements or payments, whether made in cash or otherwise;

(iv) membership subscriptions to associations or groups and arising from agreements separate from the credit agreement, even though such subscriptions have an effect on the credit terms;

(v) charges for insurance or guarantees; included are, however, those designed to ensure payment to the creditor, in the event of the death, invalidity, illness or unemployment of the consumer, of a sum equal to or less than the total amount of the credit togehter with relevant interest and other charges which have to be imposed by the creditor as a condition for credit being granted.

3. (a) Where credit transactions referred to in this Directive are subject to the provisions of national laws in force on 1 March 1990 which impose maximum limits on the annual percentage rate of charge for such transactions and, where such provisions permit standard costs other than those described in paragraph 2 (i) to (v) not to be included in those maximum limits, Member States may, solely in respect of such transactions, not include the aforementioned costs when calculating the annual percentage rate of charge, as stipulated in this Directive, provided that there is a requirement in the cases mentioned in Article 3 and in the credit agreement, that the consumer be informed of the amount and inclusion thereof in the payments to be made.

(b) Member States may no longer apply point (a) from the date of entry into force of the single mathematical formula for calculating the annual percentage rate of charge in the Community, pursuant to the provisions of paragraph 5 (c).

4. (a) The annual percentage rate of charge shall be calculated at the time the credit contract is concluded, without prejudice to the provisions of Article 3 concerning advertisements and special offers.

(b) The calculation shall be made on the assumption that the credit contract is valid for the period agreed and that the creditor and the consumer fulfil their obligations under the terms and by the dates agreed.

5. (a) As a transitional measure, notwithstanding the provisions of paragraph 1 (a), Member States which, prior to 1 March 1990, applied legal provisions whereby a mathematical formula different from that given in Annex II could be used for calculating the annual percentage rate of charge, may continue applying that formula within their territory for a period of three years starting from 1 January 1993.

Member States shall take the appropriate measures to ensure that only one mathematical formula for calculating the annual percentage rate of charge is used within their territory.

(b) Six months before the expiry of the time limit laid down in point (a) the Commission shall submit to the Council a report, accompanied by a proposal, which will make it possible in the light of experience, to apply a single Community mathematical formula for calculating the annual percentage rate of charge.

(c) The Council shall, acting by a qualified majority on the basis of the proposal from the Commission, take a decision before 1 January 1996.

6. In the case of credit contracts containing clauses allowing variations in the rate of interest and the amount or level of other charges contained in the annual percentage rate of charge but unquantifiable at the time when it is calculated, the annual percentage rate of charge shall be calculated on the assumption that interest and other charges remain fixed and will apply until the end of the credit contract.

7. Where necessary, the following assumptions may be made in calculating the annual percentage rate of charge:

—if the contract does not specify a credit limit, the amount of credit granted shall be equal to the amount fixed by the relevant Member State, without exceeding a figure equivalent to ECU 2 000;

—if there is no fixed timetable for repayment, and one cannot be deduced from the terms of the agreement and the means for repaying the credit granted, the duration of the credit shall be deemed to be one year;

—unless otherwise specified, where the contract provides for more than one repayment date, the credit will be made available and the repayments made at the earliest time provided for in the agreement’.

3. Article 2 (3) shall be replaced by the following:

‘3. The provisions of Article 1a and of Articles 4 to 12 shall not apply to credit agreements or agreements promising to grant credit, secured by mortgage on immovable property, insofar as these are not already excluded from the Directive under paragraph 1 (a).’

4. The following subparagraph shall be added to Article 4 (2):

‘(c) a statement of the amount, number and frequency or dates of the payments which the consumer must make to repay the credit, as well as of the payments for interest and other charges; the total amount of these payments should also be indicated where possible;

(d) a statement of the cost items referred to in Article 1a (2) with the exception of expenditure related to the breach of contractual obligations which were not included in the calculation of the annual percentage rate of charge but which have to be paid by the consumer in given circumstances, together with a statement indentifying such circumstances. Where the exact amount of those items is known, that sum is to be indicated; if that is not the case, either a method of calculation or as accurate an estimate as possible is to be provided where possible’.

5. Article 5 shall be deleted.

6. The Annex shall become Annex I and the following point shall be added to paragraph 1:

‘(ix) the obligation on the consumer to save a certain amount of money which must be placed in a special account’.

7. Annexes II and III attached hereto shall be added.

Article 2

1. Member States shall take the measures necessary to cumply with this Directive not later than 31 December 1992 and shall forthwith inform the Commission thereof.

2. Member States shall communicate to the Commission the texts of the main provisions of national law which they adopt in the field governed by this Directive.

Article 3

This Directive is addressed to the Member States.

Done at Brussels, 22 February 1990.

For the Council

The President

D.J. O'Malley

ANNEX

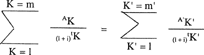

‘Annex II

THE BASIC EQUATION EXPRESSING THE EQUIVALENCE OF LOANS ON THE ONE HAND, AND REPAYMENTS AND CHARGES ON THE OTHER:

Meaning of letters and symbols:

|

K |

is the number of a loan |

|

K′ |

is the number of a repayment or a payment of charges |

|

AK |

is the amount of loan number K |

|

A′K′ |

is the amount of repayment number K′ |

|

|

represents a sum |

|

m |

is the number of the last loan |

|

m′ |

is the number of the last repayment or payment of charges |

|

tK |

is the interval, expressed in years and fractions of a year, between the date of loan No. 1 and those of subsequent loans Nos. 2 to m |

|

tK′ |

is the interval expressed in years and fractions of a year between the date of loan No. 1 and those of repayments or payments of charges Nos. 1 to m′ |

|

i |

is the percentage rate that can be calculated (either by algebra, by successive approximations, or by a computer programme) where the other terms in the equation are known from the contract or otherwise. |

Remarks

(a) The amounts paid by both parties at different times shall not necessarily be equal and shall not necessarily be paid at equal intervals.

(b) The starting date shall be that of the first loan.

(c) Intervals between dates used in the calculations shall be expressed in years or in fractions of a year.

Annex III

EXAMPLES OF CALCULATIONS

First example

Sum loaned S = ECU 1 000.

It is repaid in a single payment of ECU 1 200 made 18 months, i.e. 1,5 years, after the date of the loan.

|

The equation becomes 1000 = |

1200 _______ (1 + i)1,5 |

|

|

or (1 + i)1,5 |

= 1,2 |

|

|

1 + i |

= 1,129243 |

|

|

i |

= 0,129243 |

This amount will be rounded down to 12,9% or 12,92% depending on whether the State or habitual practice allows the percentage to be rounded off to the first or second decimal.

Second example

The sum agreed is S = ECU 1 000 but the creditor retains ECU 50 for enquiry and administrative expenses, so that the loan is in fact ECU 950; the repayment of ECU 1 200, as in the first example, is made 18 months after the date of the loan.

|

The equation becomes 950 = |

1200 _______ (1 + i)1,5 |

|

or (1 + i)1,5 |

= |

1200 ______ 950 |

= 1,263157 |

|

1 + i |

= |

1,16851 ... |

|

|

i |

= |

1,16851 ... rounded off to 16,9% or 16,85%. |

|

Third example

The sum lent is ECU 1 000, repayable in two amounts each of ECU 600, paid after one and two years respectively.

|

The equation becomes 1000 |

= |

600 _________ (1 + i) |

+ |

600 _________ (1 + i)2; |

it is solved by algebra and produces i = 0,1306623, rounded off to 13,1% or 13,07%.

Fourth example

The sum lent is ECU 1 000 and the amounts to be paid by the borrower are:

|

After three months |

(0,25 years) |

ECU 272 |

|

After six months |

(0,50 years) |

ECU 272 |

|

After twelve months (1 year) |

(1 year) |

ECU 544 |

|

_________ |

||

|

Total |

ECU 1 088 |

The equation becomes:

|

1000 |

= |

272 _________ (1 + i)0.25 |

+ |

272 _________ (1 + 0)0.50 |

+ |

544 ______ (1 + i) |

This equation allows i to be calculated by successive approximations, which can be programmed on a ocket computer.

The result is:

i = 0,1321 rounded off 13,2 or 13,21%.’

F231[Part III

DIRECTIVE 98/7/EC OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 16 February 1998

amending Directive 87/102/EEC for the approximation of the laws, regulations and administrative provisions of the Member States concerning consumer credit

THE EUROPEAN PARLIAMENT AND THE COUNCIL OF THE EUROPEAN UNION,

Having regard to the Treaty establishing the European Community, and in particular Article 100a thereof,

Having regard to the proposal of the Commission(1).

Having regard to the opinion of the Economic and Social Committee(2),

Acting in accordance with the procedure laid down in Article 189b of the Treaty(3)

Whereas it is desirable, in order to promote the establishment and functioning of the internal market and to ensure that consumers benefit from a high level of protection, that a single method of calculating the annual percentage rate of charge for consumer credit should be used throughout the Community;

Whereas Article 5 of Directive 87/102/EEC(4) provides for the introduction of a Community method or methods of calculating the annual percentage rate of charge;

Whereas, in order to introduce this single method, it is desirable to draw up a single methematical formula for calculating the annual percentage rate of charge and for determining the credit cost items to be used in the calculation by indicating those costs which must not be taken into account;

Whereas Annex II of Directive 87/102/EEC introduced a mathematical formula for the calculation of the annual percentage rate of charge and Article 1a(2) of that Directive provided for the charges to be excluded from the calculation of the ‘total cost of credit to the consumer’.

Whereas during a transitional period of three years from January 1993, Member States which prior to 1 March 1990 applied laws which permitted the use of another mathematical formula for calculating the annual percentage rate of charge, were permitted to continue to apply such laws;

Whereas the Commission has submitted a Report to the Council which makes it possible, in the light of experience, to apply a single Community mathematical formula for calculating the annual percentage rate of charge;

Whereas, since no Member State has made use of Article 1a(3) of Directive 87/102/EEC by which certain costs were excluded from the calculation of the annual percentage rate of charge in certain Member States, it has become obsolete;

Whereas accuracy to at least one decimal place is necessary;

Whereas a year is presumed to have 365 or 365,25 days or (for leap years) 366 days, 52 weeks or 12 equal months; whereas an equal month is persumed to have 30,41666 days;

Whereas it is desirable that consumers should be able to recognize the terms used different Member States to indicate the "annual percentage rate of charge";

Whereas it is appropriate to study without delay to what extent a further degree of harmonization of the cost elements of consumer credit is necessary in order to put the European consumer in a position to make a better comparison between the actual percentage rates of charges offered by institutions in the various Member State, thereby ensuring harmonious functioning of the internal market,

HAVE ADOPTED THIS DIRECTIVE:

Article 1

Directive 87/102/EEC shall be amended as follows:

(a) Article 1a(1)(a) shall be replaced by the following:

—in the Greek language version of the Directive:

...

—in the English language version of the Directive:

‘The annual percentage rate of charge which shall be that rate, on an annual basis which equalizes the present value of all commitments (loans, repayments and charges), future or existing, agreed by the creditor and the borrower, shall be calculated in accordance with the mathematical formula set out in Annex II.’;

(b) Article 1a(3) shall be deleted;

(c) Article 1a(5) shall be deleted;

(d) Article 3 shall be replaced by the following:

‘Without prejudice to Council Directive 84/450/EEC of 10 September 1984 relating to the approximation of the laws, regulations and administrative provisions of the Member States concerning misleading advertising(*), and to the rules and principles applicable to unfair advertising, any advertisement, or any offer which is displayed at business premises, in which a person offers credit or offers to arrange a credit agreement and in which a rate of interest or any figures relating to the cost of the credit are indicated, shall also include a statement of the annual percentage rate of charge, by means of a

(e) Annex II shall be replaced by the text of Annex I representative example if no other means is practicable.

attached hereto;

(f) Annex III shall be replaced by the text of Annex II attached hereto.

Article 2

1. Member States shall bring into force the laws, regulations and administrative provisions necessary for them to comply with this Directive no later than two years after the entry into force of this Directive. They shall inform the Commission thereof.

When Member States adopt those measures, they shall contain a reference to this Directive or shall be accompained by such reference on the occasion of their official publication. The methods of making such reference shall be laid down by Member States.

2. The Member States shall communicate to the Commission the texts of the provisions of national law which they adopt in the field governed by this Directive.

Article 3

This Directive is addressed to the Member States.

Done at Brussels, 16 February 1998.

|

For the European Parliament |

For the Council |

|

The President |

The President |

|

J.M. GIL-ROBLES |

J. CUNNINGHAM |

ANNEX I

‘ANNEX II

THE BASIC EQUATION EXPRESSING THE EQUIVALENCE OF LOANS ON THE ONE HAND AND REPAYMENTS AND CHARGES ON THE OTHER

Meaning of letters and symbols:

K is the number of a loan

K’ is the number of a repayment or a payment of charges

Ak is the amount of loan number K

A’k’ is the amount of repayment number K’

∑ represents a sum

m is the number of the last loan

m’ is the number of the last repayment or payment of charges

tk’ is the interval, expressed in years and fractions of a year, between the date of loan No. 1 and those of subsequent loans Nos 2 to m

tk’ is the interval, expressed in years and fractions of a year, between the date of loan No. 1 and those of repayments or payments of charges Nos 1 to m’

i is the percentage rate that can be calculated (either by algegra, by successive approximations, or by a computer programme) where the other terms in the equation are known from the contract or otherwise.

Remarks:

(a) The amounts paid by both parties at different times shall not necessarily be equal and shall not necessarily be paid at equal intervals.

(b) The starting date shall be that of the first loan.

(c) Intervals between dates used in the calculations shall be expressed in years or in fractions of a year. A year is presumed to have 365 days or 365,25 days or (for leap years) 366 days, 52 weeks or 12 equal months. An equal month is presumed to have 30,41666 days (i.e. 365/12).

(d) The result of the calculation shall be expressed with an accuracy of at least one decimal place. When rounding to a particular decimal place the following rule shall apply:

If the figure at the decimal place following this particular decimal place is greater than or equal to 5, the figure at this particular decimal place shall be increased by one.

(e) Member States shall provide that the methods of resolution applicable give a result equal to that of the examples presented in Annex III.’

ANNEX II

‘ANNEX III

EXAMPLES OF CALCULATION

A. CALCULATION OF THE ANNUAL PERCENTAGE RATE OF CHARGE ON A CALENDAR BASIS (1 YEAR = 365 DAYS (OR 366 DAYS FOR LEAP YEARS)

First example

Sum loaned: S = ECU 1000 on 1 January 1994.

It is repaid in a single payment of ECU 1200 made on 1 July 1995 i.e. 1 1/2 years or 546 (= 365 + 181) days after the date of the loan,

|

The equation becomes: 1,000 = |

1200 |

|

|

(1+ i)546/365 |

or:

(1+ i)546/365 = 1,2

1+ i = 1,1296204

i = 0,1296204

This amount will be rounded to 13% (or 12,96% if an accuracy of two decimal places is preferred).

Second example

The sum loaned is S = ECU 1,000, but the creditor retains ECU 50 for administrative expenses, so that the loan is in fact ECU 950; the repayment of ECU 1,200, as in the first example, is again made on 1 July 1995.

|

The equation becomes: 950 = |

1200 |

|

|

(1+ i)546/365 |

or:

(1+ i)546/365 = 1,263157

1+ i = 1,169026

i = 0,169026

This amount will be rounded to 16,9%.

Third example

The sum loaned is ECU 1,000, on 1 January 1994, repayable in two amounts, each ECU 600, paid after one and two years respectively.

The equation becomes:

|

1000 = |

600 |

+ |

600 |

= |

600 |

+ |

600 |

|

|

(1+ i) |

(1+ i)730/365 |

(1+ i) |

(1+ i)2 |

It is solved by algebra and produces i=0,1306623 rounded to 13,1% (or 13,07% if an accuracy of two decimal places is preferred).

Fourth example

The sum loaned is S= ECU 1,000, on 1 January 1994, and the amounts to be paid by the borrower are:

|

After 3 months (0.25 years/90 days): |

ECU 272 |

|

|

After 6 months (0.5 years/181 days): |

ECU 272 |

|

|

After 12 months (1 year/365 days): |

ECU 544 |

|

|

Total: |

ECU 1,088 |

The equation becomes:

|

1000 = |

272 |

+ |

272 |

+ |

544 |

|

|

(1+ i)90/365 |

(1+ i)181/365 |

(1+ i)365/365 |

This equation allows i to be calculated by successive approximations, which can be programmed on a pocket calculation.

The result is i=0,13226 rounded to 13.2% (or 13,23% if an accuracy of two decimal places is preferred).

B. CALCULATION OF THE ANNUAL PERCENTAGE RATE OF CHARGE ON THE BASIS OF A STANDARD YEAR (1 YEAR = 365 DAYS OR 365,25 DAYS, 52 WEEKS, OR 12 EQUAL MONTHS)

First example

Sum loaned: S = ECU 1,000

It is repaid in a single payment of ECU 1,200 made in 1.5 years (i.e. 1,5 x 365=547,5 days, 1,5 x 365,25 = 547,875 days, 1.5 x 366 = 549 days, 1,5 x 12 = 18 months, or 1,5 x 52 =78 weeks) after the date of the loan.

The equation becomes:

|

1000 = |

1,200 |

= |

1,200 |

= |

1,200 |

= |

1,200 |

|

|

(1+ i)547,5/365 |

(1+ i)547,875/365 |

(1+ i)18/12 |

(1+ i)78/52 |

or:

(1+ i)1,5 = 1,2

1+ i = 1,129243

i = 0,129243

This amount will be rounded to 12,9% (or 12,92% if an accuracy of two decimal places is preferred).

Second example

The sum loaned is S = ECU 1,000, but the creditor retains ECU 50 for administrative expenses, so that the loan is in fact ECU 950; the repayment of ECU 1,200, as in the first example, is again made 1.5 years after the date of the loan.

The equation becomes:

|

950 = |

1,200 |

= |

1,200 |

= |

1,200 |

= |

1,200 |

|

|

(1+ i)547,5/365 |

(1+ i)547,875/365 |

(1+ i)18/12 |

(1+ i)78/52 |

or:

(1+ i)1,5 = 1200/950 = 1,263157

1+ i = 1,168526

i = 0,168526

This amount will be rounded to 16.9% (or 16.85% if an accuracy of two decimal places is preferred).

Third example

The sum loaned is ECU 1,000, repayable in two amounts, each of ECU 600, paid after one and two years respectively.

The equation becomes

|

1000 = |

600 |

+ |

600 |

= |

600 |

+ |

600 |

|

|

(1+ i)365/365 |

(1+ i)730/365 |

(1+ i)365,25/365,25 |

(1+ i)730,5/365,52 |

|

= |

600 |

+ |

600 |

= |

600 |

+ |

600 |

|

|

(1+ i)12/12 |

(1+ i)24/12 |

(1+ i)52/52 |

(1+ i)104/52 |

|

= |

600 |

+ |

600 |

|

|

(1+ i)1 |

(1+ i)2 |

It is solved by algebra and produces i = 0,13066 which will be rounded to 13,1% (or 13,07% if an accuracy of two decimal places is preferred).

Fourth example

The sum loaned is S = ECU 1,000 and the amounts to be paid by the borrower are:

|

After 3 months (0,25 years/13 Weeks/91,25 days/91,3125 days): |

ECU 272 |

|

|

After 6 months (0,5 years/26 Weeks/182,5 days/182,625 days): |

ECU 272 |

|

|

After 12 months (1 year/52 weeks/365 days/365,25 days): |

ECU 544 |

|

|

Total: |

ECU 1,088 |

The equation becomes:

|

1000 = |

272 |

+ |

272 |

+ |

544 |

|

|

(1+ i)91,25/365 |

(1+ i)182,5/365 |

(1+ i)365/365 |

|

= |

272 |

+ |

272 |

+ |

544 |

|

|

(1+ i)91,3125/365,25 |

(1+ i)182,625/365,25 |

(1+ i)365,25/365,25 |

|

= |

272 |

+ |

272 |

+ |

544 |

|

|

(1+ i)3/12 |

(1+ i)6/12 |

(1+ i)12/12 |

|

= |

272 |

+ |

272 |

+ |

544 |

|

|

(1+ i)13/52 |

(1+ i)26/52 |

(1+ i)52/52 |

|

= |

272 |

+ |

272 |

+ |

544 |

|

|

(1+ i)0,25 |

(1+ i)0,5 |

(1+ i)1 |

This equation allows i to be calculated by successive approximations, which can be programmed on a pocket calculator. The result is i = 0,13185 which will be rounded to 13,2% (or 13,19% if an accuracy of two decimal places is preferred).]

Annotations

Amendments:

F231

Inserted (20.09.2000) by European Communities (Consumer Credit) Regulations 2000 (S.I. No. 294 of 2000), reg. 5 and Table part 1.