Revised Acts

This Act

Download PDFs

On the eISB

Number 24 of 1995

CONSUMER CREDIT ACT 1995

REVISED

Updated to 5 February 2026

This Revised Act is an administrative consolidation of the Consumer Credit Act 1995. It is prepared by the Law Reform Commission in accordance with its function under the Law Reform Commission Act 1975 (3/1975) to keep the law under review and to undertake revision and consolidation of statute law.

All Acts up to and including the Credit Review Act 2026 (1/2026), enacted 3 February 2026, and all statutory instruments up to and including the Gambling Regulation Act 2024 (Commencement) Order 2026 (S.I. No. 31 of 2026), made 3 February 2026, were considered in the preparation of this Revised Act.

Disclaimer: While every care has been taken in the preparation of this Revised Act, the Law Reform Commission can assume no responsibility for and give no guarantees, undertakings or warranties concerning the accuracy, completeness or up to date nature of the information provided and does not accept any liability whatsoever arising from any errors or omissions. Please notify any errors, omissions and comments by email to

revisedacts@lawreform.ie.

Number 24 of 1995

CONSUMER CREDIT ACT 1995

REVISED

Updated to 5 February 2026

ARRANGEMENT OF SECTIONS

Preliminary and General

|

Section |

|

Responsibilities and Powers of Director of Consumer Affairs

Functions and Powers of Central Bank of Ireland

Provisions applicable to Director and Bank

|

Director and Bank to be immune from certain civil proceedings. |

|

Advertising and Offering of Financial Accommodation

Annual Percentage Rate

Requirements Relating to Credit Agreements and Form and Contents thereof

Matters Arising During Currency of Agreements

|

Power of court to re-open credit agreement where charge is excessive. |

|

|

Making demands and threats in relation to unenforceable agreements. |

|

Matters Arising on Termination of Agreements or on Default

|

Reduction where amount owed becomes payable before time fixed by agreement. |

|

Hire-Purchase Agreements

Consumer-Hire Agreements

|

Regulations relating to form and content of consumer-hire agreements. |

|

|

Application of sections 73A to 83 to consumer-hire agreements. |

|

|

Duty of hirer to give information as to whereabouts of goods. |

Provisions Relating to Moneylending

Housing Loans Made by Mortgage Lenders

Miscellaneous

Credit Intermediaries

|

Obligation to display copy of credit intermediaries authorisation. |

|

|

Prohibition on alteration or falsification of credit intermediaries authorisation. |

|

Obligation on Credit Institutions to Notify Director of all Customer Charges

|

Customer charges, etc., by credit institutions that are subject to regulation by the Bank. |

|

|

Customer charges, etc. payable by persons authorised to carry on business of a bureau de change. |

|

Moneylenders, Credit and Mortgage Intermediaries Registers

|

Register of high cost credit providers and mortgage intermediaries. |

|

Amendment of Sale of Goods and Supply of Services Act, 1980

Amendment of Pawnbrokers Act, 1964

Amendment of Consumer Information Act, 1978

Number 24 of 1995

CONSUMER CREDIT ACT 1995

REVISED

Updated to 5 February 2026

AN ACT TO REVISE AND EXTEND THE LAW RELATING TO CONSUMER CREDIT, HIRE-PURCHASE, HIRING AND MONEYLENDING AND TO ENABLE EFFECT TO BE GIVEN TO COUNCIL DIRECTIVE NO. 87/102/EEC OF 22 DECEMBER, 1986, AS AMENDED BY COUNCIL DIRECTIVE NO. 90/88/EEC OF 22 FEBRUARY, 1990, AND FOR THOSE PURPOSES TO REPEAL THE HIRE-PURCHASE ACTS, 1946 TO 1980, AND THE MONEYLENDERS ACTS, 1900 TO 1989, AND TO REPEAL AND AMEND CERTAIN PROVISIONS OF THE SALE OF GOODS AND SUPPLY OF SERVICES ACT, 1980, TO PROVIDE THAT THE DIRECTOR OF CONSUMER AFFAIRS SHALL MONITOR ALL CUSTOMER CHARGES BY CREDIT INSTITUTIONS AND FOR THAT PURPOSE TO REPEAL SECTION 28 OF THE CENTRAL BANK ACT, 1989, TO PROVIDE FOR THE AMENDMENT AND EXTENSION OF THE PAWNBROKERS ACT, 1964, TO PROVIDE FOR THE AMENDMENT OF SECTION 9 OF THE CONSUMER INFORMATION ACT, 1978, AND TO PROVIDE FOR CONNECTED MATTERS. [31st July, 1995]

BE IT ENACTED BY THE OIREACHTAS AS FOLLOWS:

Annotations

Modifications (not altering text):

C1

Functions of National Consumer Agency re-transferred and references construed (31.10.2014) by Competition and Consumer Protection Act 2014 (29/2014), s. 39, S.I. No. 366 of 2014. Functions were previously transferred from Director of Consumer Affairs to National Consumer Agency, see E-note below.

Transfer of functions to Commission

39. (1) All functions that, immediately before the establishment day, were vested in the dissolved bodies are transferred to the Commission.

(2) References in any Act of the Oireachtas passed before the establishment day or in any instrument made before that day under an Act of the Oireachtas to—

(a) the National Consumer Agency, or

...

shall, on and after that day, be construed as references to the Commission.

(3) A reference in any Act of the Oireachtas passed before the establishment day or in any instrument made before that day under an Act of the Oireachtas to the chief executive of the National Consumer Agency shall, on and after that day, be construed as a reference to the chairperson of the Commission.

C2

Application of Act restricted (1.10.1997) by Credit Union Act 1997 (15/1997), s. 184(c), S.I. No. 403 of 1997, as substituted (1.08.2013) by Credit Union and Co-operation with Overseas Regulators Act 2012 (40/2012), s. 34, S.I. No. 280 of 2013.

Certain enactments not to apply to credit unions etc.

[184.— The following enactments, namely— ...

(c) the Consumer Credit Act 1995,

shall not apply to a credit union or to a body the members of which are credit unions and the principal objects of which are the promotion of the credit union movement and the provision of services to credit unions.]

Editorial Notes:

E1

Offences under Act excluded from application of Criminal Justice (Forensic Evidence and DNA Database System) Act 2014 (11/2014), s. 11 (20.11.2015) by Criminal Justice (Forensic Evidence and DNA Database System) Act 2014 (Section 11) Order 2015 (S.I. No. 527 of 2015), arts. 3, 4 and sch., in effect as per art. 1(2).

E2

Exemption of Act from application of Electronic Commerce Act 2000 by Electronic Commerce Act 2000 (27/2000), s. 11 removed (1.08.2013) by Central Bank (Supervision and Enforcement) Act 2013 (26/2013), s. 89, S.I. No. 287 of 2013.

E3

Competent authorities designated for purpose of Act (30.05.2006) by European Communities (Cooperation between National Authorities Responsible for the Enforcement of Consumer Protection Laws) Regulations 2006 (S.I. No. 290 of 2006), reg. 4(1) and sch. ref. no. 3.

E4

Act included in definition of designated enactments for purposes of Central Bank Act 1942 (22/1942), s. 2(1) and sch. 2 part 1 item 22, as substituted (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 31, S.I. No. 160 of 2003, and as subsequently substituted (1.10.2010) by Central Bank Reform Act 2010 (23/2010), s. 14(1) and sch. 1 part 1 item 82, S.I. No. 469 of 2010.

E5

Previous affecting provision: functions of Director of Consumer Affairs transferred and references construed (1.05.2007) by Consumer Protection Act (19/2007), ss. 2, 37 and sch. 1 part 1, S.I. No. 178 of 2007; repealed (31.10.2014) by Competition and Consumer Protection Act 2014 (29/2014), s. 7(2), S.I. No. 366 of 2014.

E6

Previous affecting provision: functions of Central Bank transferred and references construed by Central Bank Act (22/1942), s. 33C(1) and sch. 2, as inserted (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 26, S.I. No. 160 of 2003; substituted and deleted (1.10.2010) by Central Bank Reform Act 2010 (23/2010), s. 14(1) and sch. 1 part 1 item 39, S.I. No. 469 of 2010.

PART I

Preliminary and General

Annotations

Modifications (not altering text):

C3

Application of Part extended (1.09.1997) by Consumer Credit Act, 1995 (Section 3) Regulations 1997 (S.I. No. 186 of 1997), reg. 3, in effect as per reg. 2.

3. The following provisions of the Consumer Credit Act, 1995 (No. 24 of 1995), shall apply to a housing loan advanced by a local authority—

( a ) Part I, other than sections 9 to 16, 18 and 19, and

( b ) in Part IX, sections 115, 121 (1), other than "Subject to subsection (3),", 123, 124, 125, 128, 129, where applicable, 130, 132 and 134.

Section 1

Section 1

Short title and commencement.

1.—(1) This Act may be cited as the Consumer Credit Act, 1995.

(2) This Act shall come into operation on such day or days as the Minister may appoint by order or orders either generally or with reference to any particular purpose or provision and different days may be so appointed for different purposes and different provisions.

Annotations

Editorial Notes:

E7

Power pursuant to subs. (2) exercised (13.05.1996) by Consumer Credit Act, 1995 (Commencement) Order 1996 (S.I. No. 121 of 1996).

2. The 13th day of May, 1996, is hereby appointed as the day on which the Consumer Credit Act, 1995 (No. 24 of 1995), other than section 54 (3) thereof, shall come into operation.

Section 2

Interpretation.

2.—(1) In this Act, unless the context otherwise requires—

"the Act of 1980" means the Sale of Goods and Supply of Services Act, 1980;

F1["Act of 1997" means the Central Bank Act 1997;]

F2["Act of 2022" means the Consumer Rights Act 2022;]

F3["Act of 2024" means the Gambling Regulation Act 2024;]

"advertisement" includes every form of advertising, whether in a publication, by television or radio, by display of notices, signs, labels, showcards or goods, by distribution of samples, circulars, catalogues, price lists or other material, by exhibition of pictures, models or films, or in any other way, and references to the publishing of advertisements shall be construed accordingly;

"agreement" means an agreement to which this Act applies;

F4["APR" means the annual percentage rate of charge (being, in the case of a credit agreement, the total cost of credit to the consumer, expressed as an annual percentage of the amount of credit granted), calculated in accordance with section 9;]

F5[…]

F5[…]

F6["Bank" means the Central Bank F7[…];]

"borrower" means a consumer acting as a borrower;

F8["business" includes trade and profession;]

"business name" means the name or style under which any business is carried on;

"buyer" means a consumer acting as a buyer;

"cash" includes money in any form;

"cash price" means the money consideration for a transaction for the purchase of goods or the supply of a service by a consumer which is not financed by credit;

F5[…]

"collecting repayments" means, in respect of a F9[high cost credit agreement], the collection of repayments in respect of the agreement at a place other than a business premises of the F9[high cost credit provider];

"company" means—

(a) a company within the meaning of the Companies Acts, 1963 to 1990, or

(b) a body established under the laws of a state other than the State and corresponding to a body referred to in paragraph (a);

F2["commercial guarantee", in relation to a hire-purchase agreement, means any undertaking by an owner or producer to a hirer (in addition to the owner’s legal obligation to supply goods in conformity with the agreement) to reimburse the price paid or to repair, replace or service goods in any way if they do not meet the specifications or any other requirements not related to conformity set out in the guarantee statement or in the relevant advertising available at the time of, or before, the conclusion of the hire-purchase agreement;

"compatibility" means the ability of goods to function with hardware or software with which goods of the same type are normally used without the need to convert the goods, hardware or software;]

F10["consumer" means—

(a) a natural person acting outside the person's business, or

(b) any person, or person of a class, declared to be a consumer in an order made under subsection (9);]

"consumer-hire agreement" means an agreement of more than three months duration for the bailment of goods to a hirer under which the property in the goods remains with the owner;

"contract of guarantee" means, in relation to any agreement, a contract, made at the request express or implied of the consumer, to guarantee the performance of the consumer's obligations under the agreement, and the expression "guarantor" shall be construed accordingly;

"cooling-off period" has the meaning assigned to it by section 50;

"the Council Directive" means Council Directive No. 87/102/EEC of 22 December 1986(1), for the approximation of the laws, regulations and administrative provisions of the Member States of the European Communities concerning consumer credit, F11[as amended by Council Directive No. 90/88/EEC of 22 February 1990(2) and Directive 98/7/EC of the European Parliament and of the Council of 16 February 1998(3), the texts of which are set out for convenience of reference F11[in Parts I, II and III, respectively, of the First Schedule;]

"credit" includes a deferred payment, cash loan F12[or other similar financial accommodation];

"credit agreement" means an agreement whereby a creditor grants or promises to grant to a consumer a credit in the form of a deferred payment, a cash loan or other similar financial accommodation;

"credit card" means a card issued by a credit institution or other person to an individual by means of which goods, services or cash may be obtained by the individual on credit and amounts in respect of the goods, services or cash may be charged to the credit card account of the individual maintained by the credit institution or other person;

"credit institution" means—

(a) the holder of a licence granted under section 9 of the Central Bank Act, 1971,

(b) a body licensed to carry on banking under regulations made under the European Communities Act, 1972,

(c) a building society incorporated or deemed to be incorporated under section 10 of the Building Societies Act, 1989,

(d) a society licensed to carry on the business of a trustee savings bank under section 10 of the Trustee Savings Banks Act, 1989,

F13[(e) a retail credit firm authorised under the Act of 1997;]

(f) F14[…]

(g) F5[…]

"credit intermediary" means a person, other than a credit institution or a mortgage lender, who in the course of his business arranges or offers to arrange for a consumer the provision of credit or the letting of goods in return for a commission, payment or consideration of any kind from the provider of the credit or the owner, as the case may be;

"credit intermediaries authorisation" means an authorisation granted under section 144;

"credit-sale agreement" means a credit agreement for the sale of goods under which the purchase price or part of it is payable in instalments and the property in the goods passes to the buyer immediately upon the making of the agreement;

"creditor" means a person who grants credit under a credit agreement in the course of his trade, business or profession, and includes a group of such persons;

F2["delivery" means voluntary transfer of possession from one person to another;

"digital content" has the meaning assigned to it by the Act of 2022;

"digital service" means—

(a) a service that allows a hirer to create, process, store or access data in digital form, or

(b) a service that allows the sharing of or any other interaction with data in digital form uploaded or created by a hirer or any other user of the service,

and includes in particular video and audio sharing and other file hosting, social media and word processing and games offered in the cloud computing environment;]

"the Director" means the Director of Consumer Affairs;

"financial accommodation" includes credit and the letting of goods;

"functions" includes powers and duties;

F2["functionality" means the ability of goods to perform their functions having regard to their purpose;

"goods" has the meaning assigned to it by the Act of 2022;

"goods with digital elements" has the meaning assigned to it by the Act of 2022;

"guarantor" means—

(a) an owner,

(b) a producer, or

(c) any other person who provides a commercial guarantee in relation to goods let under a hire-purchase agreement;]

F15["high cost credit" means credit supplied by a high cost credit provider to a consumer on foot of a high cost credit agreement;

"high cost credit agreement" means a credit agreement into which a high cost credit provider enters, or offers to enter, with a consumer in which one or more of the following apply:

(a) the agreement was concluded away from the business premises of the high cost credit provider or the business premises of the supplier of goods or services under the agreement;

(b) any negotiations for, or in relation to the credit were conducted at a place other than the business premises of the high cost credit provider or the business premises of the supplier of goods or services under the agreement;

(c) repayments under the agreement will, or may, be paid by the consumer to the high cost credit provider or the representative of the high cost credit provider at any place other than the business premises of the high cost credit provider or the business premises of the supplier of goods or services under the agreement;

(d) the total cost of credit to the consumer under the agreement is in excess of an APR of 23 per cent, or such other rate as may be prescribed;

"high cost credit provider" means a person who engages in the provision of high cost credit, or who advertises or announces themselves or holds themselves out in any way as engaging in the provision of high cost credit, but does not include—

(a) any pawnbroker in respect of business carried on by the pawnbroker in accordance with the provisions of the Pawnbrokers Act 1964 ,

(b) a society which is registered as a credit union under the Credit Union Act 1997,

(c) a registered society within the meaning of the Friendly Societies Acts 1896 to 2021,

(d) a credit institution,

(e) a person who supplies money for the purchase, sale or hire of goods at an APR which is less than or equal to 23 per cent (or such other rate as may be prescribed), or

(f) a mortgage lender;

"high cost credit provider’s licence" means a licence granted under section 93;]

"hirer" means a consumer who takes, intends to take or has taken goods from an owner under a hire-purchase agreement or a consumer-hire agreement in return for periodical payments;

"hire-purchase agreement" means an agreement for the bailment of goods under which the hirer may buy the goods or under which the property in the goods will, if the terms of the agreement are complied with, pass to the hirer in return for periodical payments; and where by virtue of two or more agreements, none of which by itself constitutes a hire-purchase agreement, there is a bailment of goods and either the hirer may buy the goods, or the property therein will, if the terms of the agreements are complied with, pass to the hirer, the agreements shall be treated for the purpose of this Act as a single agreement made at the time when the last agreement was made;

"house" includes any building or part of a building used or suitable for use as a dwelling and any outoffice, yard, garden or other land appurtenant thereto or usually enjoyed therewith;

F10["housing loan" means—

(a) an agreement for the provision of credit to a person on the security of a mortgage of a freehold or leasehold estate or interest in land—

(i) for the purpose of enabling the person to have a house constructed on the land as the principal residence of that person or that person's dependants, or

(ii) for the purpose of enabling the person to improve a house that is already used as the principal residence of that person or that person's dependants, or

(iii) for the purpose of enabling the person to buy a house that is already constructed on the land for use as the principal residence of that person or that person's dependants,

or

(b) an agreement for refinancing credit provided to a person for a purpose specified in paragraph (a)(i), (ii) or (iii), or

(c) an agreement for the provision of credit to a person on the security of a mortgage of a freehold or leasehold estate or interest in land on which a house is constructed where the house is to be used, or to continue to be used, as the principal residence of the person or the person's dependants, or

(d) an agreement for the provision of credit to a person on the security of a mortgage of a freehold or leasehold estate or interest in land on which a house is, or is to be, constructed where the person to whom the credit is provided is a consumer;]

"installation charge" means the charge for—

(a) the installing of any electric line or any gas or water pipe,

(b) the fixing of goods to which the agreement relates to the premises where they are to be used, and the alteration of premises to enable any such goods to be used thereon, and

(c) where it is reasonably necessary that any such goods should be constructed or erected on the premises where they are to be used, any work carried out for the purpose of such construction or erection;

F6["local authority" means a local authority for the purposes of the Local Government Act 2001;]

F5[…]

F16[…]

F16[…]

F16[…]

F16[…]

"mortgage" includes charge;

F10["mortgage lender" means a person who carries on a business that consists of or includes making housing loans;]

F17["mortgage intermediary" means a person (other than a mortgage lender or credit institution) who, in return for commission or some other form of consideration—

(a) arranges, or offers to arrange, for a mortgage lender to provide a consumer with a housing loan, or

(b) introduces a consumer to an intermediary who arranges, or offers to arrange, for a mortgage lender to provide the consumer with such a loan;]

"motor vehicle" means a vehicle intended or adapted for propulsion by mechanical means;

"owner" means the person who lets or has let goods to a hirer under a hire-purchase agreement or a consumer-hire agreement;

"partnership" has the meaning assigned to it by the Partnership Act, 1890;

F6["pawnbroker" means the holder of a licence granted under section 8 of the Pawnbrokers Act 1964;]

"premises" includes any building, dwelling, temporary construction, vehicle, ship or aircraft;

"prescribed" means prescribed by regulations F18[made under this Act] and "prescribe" shall be construed accordingly;

F2["producer" means—

(a) a manufacturer of goods,

(b) an importer of goods into the European Union, or

(c) any person purporting to be a producer by placing the person’s name, trade mark or other distinctive sign on the goods, and includes any person acting in the name, or on behalf, of the producer;]

"record" means any book, document or any other written or printed material in any form including any information stored, maintained or preserved by means of any mechanical or electronic device, whether or not stored, maintained or preserved in a legible form;

F7[…]

F1["relevant date" means the date on which section 14 of the Consumer Protection (Regulation of Retail Credit and Credit Servicing Firms) Act 2022 comes into operation;]

F1["retail credit firm" has the same meaning as it has in Part V of the Act of 1997;]

F5[…]

"running account" means a facility under a credit agreement whereby the consumer is enabled to receive, from time to time, from the creditor or a third party, cash, goods or services to an amount or value such that, taking into account payments made by or to the credit of the consumer, the credit limit (if any) is not at any time exceeded;

"total cost of credit" means the total cost of the credit to the consumer being all the costs, comprising interest, collection and all other charges, which the consumer has to pay for the credit exclusive of any sum payable as a penalty or as compensation or damages for breach of the agreement;

"undertaking" means a company, partnership or any other person.

(2) In this Act a reference to a borrower, buyer, consumer, creditor, hirer, owner or seller includes a person to whom the borrower's, buyer's, consumer's, creditor's, hirer's, owner's or seller's rights or liabilities, as the case may be, under an agreement have passed by assignment or operation of law.

(3) In this Act a reference to a section, Part or Schedule, is a reference to a section or Part of, or Schedule to this Act, unless there is an indication that a reference to any other enactment is intended or otherwise indicated.

(4) In this Act a reference to a subsection, paragraph or subparagraph is a reference to the subsection, paragraph or subparagraph of the provision in which the reference occurs, unless there is an indication that a reference to some other provision is intended.

(5) Any reference in this Act to a term of an agreement includes a reference to a term which although not contained in an agreement is incorporated in the agreement by another term of the agreement.

(6) A word or expression that is used in this Act and is also used in the Council Directive has, unless the contrary intention appears, the meaning in this Act that it has in the Council Directive.

(7) In construing a provision of this Act, a court shall give to it a construction that will give effect to the Council Directive, and for this purpose a court shall have regard to the provisions of the Council Directive, including the preambles.

(8) In this Act a reference to any enactment shall be construed as a reference to that enactment as amended or adapted by or under any subsequent enactment.

F8[(9) The Minister for Finance may, by order notified in Iris Oifigiúil, declare any specified person, or any person of a specified class of persons, to be a consumer for the purposes of the definition of "consumer" in subsection (1).]

F19[(10) In Part VI, a reference to a reasonable expectation shall be interpreted having regard objectively to the nature and purpose of the hire-purchase agreement, the circumstances of the case and the usages and practices of the parties to the agreement.]

Annotations

Amendments:

F1

Inserted (16.05.2022) by Consumer Protection (Regulation of Retail Credit and Credit Servicing Firms) Act 2022 (5/2022), s. 10(a), S.I. No. 229 of 2022.

F2

Substituted (29.11.2022) by Consumer Rights Act 2022 (37/2022), s. 148, S.I. No. 596 of 2022.

F3

Inserted (5.02.2026) by Gambling Regulation Act 2024 (35/2024), s. 266(1)(a), S.I. No. 31 of 2026, art. 2(i)(iii)(IV).

F4

Substituted (16.05.2022) by Consumer Protection (Regulation of Retail Credit and Credit Servicing Firms) Act 2022 (5/2022), s. 10(b), S.I. No. 229 of 2022.

F5

Deleted (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 35(1) and sch. 1 part 21 item 1, S.I. No. 160 of 2003.

F6

Inserted (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 35(1) and sch. 1 part 21 item 1, S.I. No. 160 of 2003.

F7

Deleted (1.10.2010) by Central Bank Reform Act 2010 (23/2010), s. 15(4) and sch. 2 part 4 items 1 and 2, S.I. No. 469 of 2010.

F8

Inserted (1.08.2004) by Central Bank and Financial Services Authority of Ireland Act 2004 (21/2004), s. 33 and sch. 3 part 12 item 1(a), (e), S.I. No. 455 of 2004.

F9

Substituted (14.11.2022) by Consumer Credit (Amendment) Act 2022 (13/2022), s. 15(1) and sch. 1 part 1 item 6, S.I. No. 575 of 2022.

F10

Substituted (1.08.2004) by Central Bank and Financial Services Authority of Ireland Act 2004 (21/2004), s. 33 and sch. 3 part 12 item 1(b), (ba), (d), S.I. No. 455 of 2004.

F11

Substituted (20.09.2000) by European Communities (Consumer Credit) Regulations 2000 (S.I. No. 294 of 2000), reg. 3.

F12

Substituted (23.09.1996) by European Communities (Consumer Credit Act, 1995) (Amendment) Regulations 1996 (S.I. No. 277 of 1996), reg. 2(a).

F13

Substituted (16.05.2022) by Consumer Protection (Regulation of Retail Credit and Credit Servicing Firms) Act 2022 (5/2022), s. 10(c), S.I. No. 229 of 2022.

F14

Deleted (12.02.2001) by ICC Bank Act 2000 (32/2000), s. 7(1) and sch. part 1, S.I. No. 46 of 2001.

F15

Inserted (14.11.2022) by Consumer Credit (Amendment) Act 2022 (13/2022), s. 2(b), S.I. No. 575 of 2022.

F16

Deleted (14.11.2022) by Consumer Credit (Amendment) Act 2022 (13/2022), s. 2(a), S.I. No. 575 of 2022.

F17

Substituted (1.01.2005) by Central Bank and Financial Services Authority of Ireland Act 2004 (21/2004), s. 33 and sch. 3 part 12 item 1(c), S.I. No. 455 of 2004.

F18

Substituted (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 35(1) and sch. 1 part 21 item 1, S.I. No. 160 of 2003.

F19

Inserted (29.11.2022) by Consumer Rights Act 2022 (37/2022), s. 148(b), S.I. No. 596 of 2022.

Modifications (not altering text):

C4

Definition of mortgage lender construed (13.05.1996) by Consumer Credit Act, 1995 (Section 2) Regulations 1996 (S.I. No. 127 of 1996) reg. 3.

3. The definition of "mortgage lender" contained in section 2 (1) of the Consumer Credit Act, 1995 shall include—

( a ) a person whose business includes the making of housing loans, provided that at least 50 per cent. by number of all business loans outstanding to him, in whole or in part, at any time comprises loans secured by mortgage of residential property, and

( b ) a local authority (within the meaning of the Local Government Act, 1941 ).

Editorial Notes:

E8

Power pursuant to subs. (1) exercised (3.12.1996) by Consumer Credit Act, 1995 (Section 2) (No. 2) Regulations 1996 (S.I. No. 369 of 1996).

E9

Power pursuant to subs. (1) exercised (31.07.2015) by Consumer Credit Act 1995 (Section 2) Regulations 2015 (S.I. No. 352 of 2015).

E10

Power pursuant to subs. (1) exercised (25.07.2014) by Consumer Credit Act 1995 (Section 2) (No. 1) Regulations 2014 (S.I. No. 355 of 2014).

E11

Power pursuant to subs. (1) exercised (15.08.2012) by Consumer Credit Act 1995 (Section 2) (No. 1) Regulations 2012 (S.I. No. 322 of 2012).

E12

Power pursuant to subs. (1) exercised (22.11.2010) by Consumer Credit Act 1995 (Section 2) (No. 1) Regulations 2010 (S.I. No. 551 of 2010).

E13

Power pursuant to subs. (1) exercised (30.04.2008) by Consumer Credit Act 1995 (Section 2) (No. 1) Regulations 2008 (S.I. No. 125 of 2008), in effect as per reg. 2.

E14

Power pursuant to subs. (1) exercised (23.03.2007) by Consumer Credit Act 1995 (Section 2) (No. 2) Regulations 2007 (S.I. No. 138 of 2007).

E15

Power pursuant to subs. (1) exercised (21.12.2006) by Consumer Credit Act 1995 (Section 2) (No. 1) Regulations 2006 (S.I. No. 687 of 2006).

E16

Power pursuant to subs. (1) exercised (16.11.2004) by Consumer Credit Act 1995 (Section 2) (No. 3) Regulations 2004 (S.I. No. 715 of 2004).

E17

Power pursuant to subs. (1) exercised (9.04.2002) by Consumer Credit Act 1995 (Section 2 Regulations 2002 (S.I. No. 142 of 2002).

E18

Power pursuant to subs. (1) exercised (7.12.1999) by Consumer Credit Act, 1995 (section 2) (No. 2) Regulations 1999 (S.I. No. 392 of 1999).

E19

Power pursuant to subs. (1) exercised (3.12.1996) by Consumer Credit Act, 1995 (Section 2) (No. 2) Regulations 1996 (S.I. No. 369 of 1996).

E20

Power pursuant to subs. (1) exercised (13.05.1996) by Consumer Credit Act, 1995 (Section 2) Regulations 1996 (S.I. No. 127 of 1996).

E21

Previous affecting provision: power pursuant to subs. (1) exercised (24.09.2007) by Consumer Credit Act 1995 (Section 2) (No. 4) Regulations 2007 (S.I. No. 690 of 2007); revoked (15.08.2012) by Consumer Credit Act 1995 (Section 2) (No. 1) Regulations 2012 (S.I. No. 322 of 2012), reg. 5.

E22

Previous affecting provision: power pursuant to subs. (1) exercised (14.05.2007) by Consumer Credit Act 1995 (Section 2) (No. 4) Regulations 2007 (S.I. No. 751 of 2007); revoked (15.08.2012) by Consumer Credit Act 1995 (Section 2) (No. 1) Regulations 2012 (S.I. No. 322 of 2012), reg. 5.

E23

Previous affecting provision: power pursuant to subs. (1) exercised (30.03.2007) by Consumer Credit Act 1995 (Section 2) (No. 3) Regulations 2007 (S.I. No. 139 of 2007); revoked (15.08.2012) by Consumer Credit Act 1995 (Section 2) (No. 1) Regulations 2012 (S.I. No. 322 of 2012), reg. 5.

E24

Previous affecting provision: power pursuant to subs. (1) exercised (5.03.2007) by Consumer Credit Act 1995 (Section 2) (No. 1) Regulations 2007 (S.I. No. 100 of 2007); revoked (25.07.2014) by Consumer Credit Act 1995 (Section 2) (No. 1) Regulations 2014 (S.I. No. 355 of 2014), reg. 3.

E25

Previous affecting provision: power pursuant to subs. (1) exercised (20.07.2005) by Consumer Credit Act 1995 (Section 2) (Amendment) Regulations 2005 (S.I. No. 372 of 2005); this SI amended S.I. No. 414 of 2004 and became obsolete on its revocation, see E-note below.

E26

Previous affecting provision: power pursuant to subs. (1) exercised (20.07.2005) by Consumer Credit Act 1995 (Section 2) (No. 1) Regulations 2005 (S.I. No. 371 of 2005); revoked (15.08.2012) by Consumer Credit Act 1995 (Section 2) (No. 1) Regulations 2012 (S.I. No. 322 of 2012), reg. 5.

E27

Previous affecting provision: power pursuant to subs. (1) exercised (1.07.2004) by Consumer Credit Act 1995 (Section 2) (No. 2) Regulations 2004 (S.I. No. 414 of 2004); revoked (31.07.2015) by Consumer Credit Act 1995 (Section 2) Regulations 2015 (S.I. No. 352 of 2015), reg. 3.

E28

Previous affecting provision: power pursuant to subs. (1) exercised (4.03.2004) by Consumer Credit Act 1995 (Section 2) (No. 1) Regulations 2004 (S.I. No. 93 of 2004); revoked (30.04.2008) by Consumer Credit Act 1995 (Section 2) (No. 1) Regulations 2008 (S.I. No. 125 of 2008), reg. 5, in effect as per reg. 2.

E29

Previous affecting provision: subs. (e) inserted (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 35(1) and sch.1 part 21 item 1(d), S.I. No. 160 of 2003; substituted as per F-note above.

E30

Previous affecting provision: definition of “regulatory authority” inserted (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 35(1) and sch. 1 part 21 item 1(j), S.I. No. 160 of 2003; deleted as per F-note above.

E31

Previous affecting provision: power pursuant to subs. (1) exercised (3.07.2002) by Consumer Credit Act 1995 (Section 2 (No. 2) Regulations 2002 (S.I. No. 339 of 2002); revoked (30.04.2008) by Consumer Credit Act 1995 (Section 2) (No. 1) Regulations 2008 (S.I. No. 125 of 2008), reg. 5, in effect as per reg. 5.

E32

Previous affecting provision: definition of "creditit institution", para. (e) deleted (28.02.2002) by ACC Bank Act 2001 (12/2001), s. 12(1) and sch. part 1, S.I. No. 69 of 2002; substituted (16.05.2022) as per F-note above.

E33

Previous affecting provision: power pursuant to subs. (1) exercised (21.09.2001) by Consumer Credit Act, 1995 (Section 2) Regulations 2001 (S.I. No. 432 of 2001); revoked (15.08.2012) by Consumer Credit Act 1995 (Section 2) (No. 1) Regulations 2012 (S.I. No. 322 of 2012), reg. 5.

E34

Previous affecting provision: power pursuant to subs. (1) exercised (20.04.2000) by Consumer Credit Act, 1995 (Section 2) Regulations 2000 (S.I. No. 113 of 2000); revoked (30.04.2008) by Consumer Credit Act 1995 (Section 2) (No. 1) Regulations 2008 (S.I. No. 125 of 2008), reg. 5, in effect as per reg. 2.

E35

Previous affecting provision: power pursuant to subs. (1) exercised (27.01.1999) by Consumer Credit Act, 1995 (section 2) Regulations 1999 (S.I. No. 15 of 1999); revoked (25.07.2014) by Consumer Credit Act 1995 (Section 2) (No. 1) Regulations 2014 (S.I. No. 355 of 2014), reg. 3.

E36

Power pursuant to subs. (1) exercised (13.05.1996) by Consumer Credit Act, 1995 (Section 2) Regulations 1996 (S.I. No. 127 of 1996); revoked (15.08.2012) by Consumer Credit Act 1995 (Section 2) (No. 1) Regulations 2012 (S.I. No. 322 of 2012), reg. 3.

Section 3

Application.

3.—(1) F20[Subject to this Act,] this Act shall apply to all credit agreements, hire-purchase agreements and consumer-hire agreements to which a consumer is a party.

(2) This Act shall not apply to the following, that is to say—

(a) a credit agreement in relation to credit granted or intended to be granted by—

(i) a society which is registered as a credit union under the Industrial and Provident Societies Acts, 1893 to 1978, by virtue of the Credit Union Act, 1966,

(ii) any registered society within the meaning of the Friendly Societies Acts, 1896 to 1977,

F21[except where the interest of the credit union or registered society in all or any part of the credit concerned has been directly or indirectly assigned or otherwise disposed of to any person that is not a credit union or registered society,]

F22[(aa) any transaction or proposed transaction conducted in the course of relevant trading operations within the meaning of section 39A (inserted by section 17 of the Finance Act, 1981) of the Finance Act, 1980, or within the meaning of section 39B (inserted by section 30 of the Finance Act, 1987) of the Finance Act, 1980.]

(b) a credit agreement in the form of an authentic act signed before a notary public or a judge,

F23[(c) any transaction entered into by a pawnbroker in respect of a pledge on which a loan or advance is made or to be made, or anything done with a view to such a transaction being entered into,]

(d) an agreement for the provision on a continuing basis of a service or a utility where the consumer has the right to pay for it, by means of instalments or deferred payments,

F24[(e) credit granted or made available without payment of interest or any other charge, other than where such credit is granted or made available by a person who has invited, by way of advertisement, consumers to avail of such credit,]

F25[(ea) payments of ancillary State support advanced by the Health Service Executive under the Nursing Homes Support Scheme Act 2009,]

(f) a credit agreement other than a credit agreement operated by means of a credit card under which no interest is charged provided the consumer agrees to repay the credit in a single payment, or

(g) a credit agreement between an employer and an employee made on terms which are more favourable to the employee than terms offered generally to the public in the normal course of business.

(3) F23[(a) The provisions of this Act may be applied to housing loans advanced by a local authority only by regulations made by the Minister for Finance after consultation with the Minister for the Environment and Local Government. Different provisions may be applied at different times to different classes of loans, by reference to such matters as that Minister considers appropriate.]

(b) A loan, not secured by mortgage, made by a local authority for the purposes of carrying out improvement works (within the meaning of section 1 of the Housing (Miscellaneous Provisions) Act, 1979) to a house shall be regarded as a housing loan (within the meaning of this Act) for the purposes of this Act.

Annotations

Amendments:

F20

Substituted (23.09.1996) by European Communities (Consumer Credit Act, 1995) (Amendment) Regulations 1996 (S.I. No. 277 of 1996), reg. 2(b).

F21

Inserted (8.07.2015) by Consumer Protection (Regulation of Credit Servicing Firms) Act 2015 (21/2015), s. 8, commenced on enactment.

F22

Inserted (9.04.1997) by Central Bank Act 1997 (8/1997), s. 60, S.I. No. 150 of 1997.

F23

Substituted (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 35(1) and sch. 1 part 21 item 2, S.I. No. 160 of 2003.

F24

Substituted (16.05.2022) by Consumer Protection (Regulation of Retail Credit and Credit Servicing Firms) Act 2022 (5/2022), s. 11, S.I. No. 229 of 2022.

F25

Inserted (27.10.2009) by Nursing Homes Support Scheme Act 2009 (15/2009), s. 37, S.I. No. 423 of 2009.

Editorial Notes:

E37

Power pursuant to subs. (3)(a) exercised (1.09.1997) by Consumer Credit Act, 1995 (Section 3) Regulations 1997 (S.I. No. 186 of 1987), in effect as per reg. 2.

F26[PART IA

Responsibilities and Powers of Director of Consumer Affairs]

Annotations

Amendments:

F26

Inserted (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 35(1) and sch. 1 part 21 item 3, S.I. No. 160 of 2003.

Section 4

F27[Interpretation: Part IA.

4.—(1) In this Part—

"authorised officer" means an authorised officer appointed under section 8A;

"designated provisions" means the provisions of this Act referred to in subsection (2);

"Minister" means the Minister for Enterprise, Trade and Employment;

"responsible authority" means the Minister or the Director, as appropriate.

(2) The provisions of this Act designated for the purposes of this Part are—

(a) this Part and Part XI, and

(b) Parts II, X and XIII in so far as they apply to credit intermediaries, and

(c) such other provisions of this Act as are ancillary to those Parts.]

Annotations

Amendments:

F27

Substituted (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 35(1) and sch. 1 part 21 item 3, S.I. No. 160 of 2003.

Section 5

F28[Functions of Director.

5.—(1) The Director has the following functions for the purposes of this Act:

(a) to keep under general review practices or proposed practices in relation to any of the obligations imposed on persons by or under the designated provisions;

(b) to carry out investigations of any such practices or proposed practices whenever the Director considers it in the public interest to do so or the Minister so requests;

(c) to request persons engaging in or proposing to engage in such practices as are, or are likely to be, contrary to the obligations imposed on them by any designated provision to discontinue or not engage in those practices;

(d) whenever a person in relation to whom such a request has been made engages in or is proposing to engage in any such practice, to bring civil proceedings in the High Court for an order requiring the person to discontinue or not to engage in the practice;

(e) to investigate complaints concerning possible breaches of any of the designated provisions, but at the same time having regard to the availability of other procedures for resolving those complaints;

(f) to publish codes of practice setting out conduct regarding agreements to which the designated provisions apply, in order to secure transparency and fair- ness in relation to the terms of those agreements and the conduct of agents dealing with consumers under those contracts;

(g) to perform or exercise such other functions as are imposed or conferred on the Director by this or any other Act.

(2) The Director may provide in response to complaints or otherwise, information or advice to consumers concerning agreements to which the designated provisions apply, and, in particular, on the obligations imposed on creditors or other persons by those provisions.]

Annotations

Amendments:

F28

Substituted (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 35(1) and sch. 1 part 21 item 3, S.I No. 160 of 2003.

Section 6

F29[Director to report and provide information to Minister.

6.—(1) The Director shall, not more than 3 months after the end of each year, present a report to the Minister of the Director's activities in that year in relation to the performance of the Director's functions under this Act.

(2) The Minister shall arrange for a copy of the report to be laid before each House of the Oireachtas within 2 months after receiving it.

(3) The Director shall provide the Minister with such information regarding the performance or exercise of the Director's functions under this Act as the Minister may from time to time require.]

Annotations

Amendments:

F29

Substituted (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 35(1) and sch. 1 part 21 item 3, S.I. No. 160 of 2003.

Section 7

F30[Powers of Director in respect of investigations.

7.—(1) In conducting an investigation under the designated provisions, the Director may—

(a) require any person who, in the opinion of the Director is in possession of information, or has or has access to a record or thing, that is relevant to the investigation to provide the information, record or thing to the Director, and

(b) where appropriate, require the person to attend before the Director for that purpose.

(2) A person to whom a requirement is made under this section shall comply with the requirement, but in doing so is entitled to the same immunities and privileges as if the person were a witness before a court.

(3) A person shall not obstruct or impede the Director in the performance or exercise of the Director's functions under this Act.]

Annotations

Amendments:

F30

Substituted (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 35(1) and sch. 1 part 21 item 3, S.I. No. 160 of 2003.

Section 8

F31[Directions of Director in respect of statements and notices.

8.—(1) The Director may, in the interests of better informing consumers, give directions as to the location and size of any statement or notice required under the designated provisions. The directions may be given in such manner as the Director thinks fit.

(2) A person to whom such a direction is given shall comply with that direction.]

Annotations

Amendments:

F31

Substituted (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 35(1) and sch. 1 part 21 item 3, S.I. No. 160 of 2003.

Section 8A

F32[Appointment of authorised officers for purposes of this Part.

8A.—(1) A responsible authority may in writing appoint persons to be authorised officers for the purposes of all or any of the designated provisions.

(2) An appointment under this section may be for a specified or unspecified period.

(3) A responsible authority who appoints an authorised officer shall provide the officer with a certificate of authority.

(4) Whenever an authorised officer is requested to do so by a person in relation to whom the officer is exercising a power under the designated provisions, the officer shall produce the officer's certificate of authority together with some form of personal identification.

(5) The appointment of a person as an authorised officer ends—

(a) when the responsible authority concerned revokes the appointment or the person dies or resigns from the appointment, or

(b) if the appointment is for a fixed period, when the period ends, or

(c) if the person appointed is employed in the office of that responsible authority, when the person ceases to be so employed.]

Annotations

Amendments:

F32

Inserted (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 35(1) and sch. 1 part 21 item 3, S.I. No. 160 of 2003, subject to transitional provision in s. 36 and sch. 3 para. 22.

Section 8B

F33[Powers of authorised officers under this Part.

8B.—(1) An authorised officer may, for the purpose of carrying out an investigation under this Part, do all or any of the following:

(a) at all reasonable times enter any premises, at which there are reasonable grounds to believe that—

(i) a trade or business, or any activity relating to a trade or business, is, or has been, carried on, or

(ii) records relating to a trade, business or activity are kept;

(b) search and inspect premises entered under paragraph (a) and any records on the premises;

(c) secure the premises or part of the premises for later inspection, or any part of the premises in which the officer reasonably believes records relating to a trade or business are kept;

(d) require any person who carries on a trade, business or related activity, or any person employed in or in connection with it—

(i) to produce to the officer records relating to the trade, business or activity, and

(ii) if the information is in a non-legible form, to reproduce it in a legible form or to give to the officer such information as the officer reasonably requires in relation to entries in the records;

(e) inspect and take copies of records inspected or produced under this section (including in the case of information in a non-legible form, a copy of all or part of the information in a permanent legible form);

(f) remove and retain the records inspected or produced under this section for such period as may be reasonable to facilitate further examination (subject to the issue of a warrant for that purpose by a judge of the District Court);

(g) require any such person to give to the officer information that the officer reasonably requires in relation to the trade, business or activity concerned, or in relation to the persons carrying on that trade, business or activity or employed in or in connection with it;

(h) require any such person to give to the officer any other information which the officer may reasonably require in regard to the trade, business or activity concerned;

(i) require any person by or on whose behalf data equipment is or has been used, or any person who has charge of, or is otherwise concerned with the operation of, the equipment or any associated apparatus or material, to give the officer all reasonable assistance in relation to the equipment, apparatus or material;

(j) require any other person employed in or in connection with the trade, business or activity concerned to give to the officer, at any reasonable time, information that the officer reasonably requires in relation to that trade, business or activity and to produce to the officer any records that the person has or has access to.

(2) An authorised officer shall not, except with the consent of the occupier, enter a private dwelling unless the officer has obtained a warrant from the District Court under section 8C authorising the entry.]

Annotations

Amendments:

F33

Inserted (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 35(1) and sch. 1 part 21 item 3, S.I. No. 160 of 2003.

Section 8C

F34[Issue of search warrants.

8C.—(1) If an authorised officer is prevented from entering premises under section 8B, the officer or another authorised officer may apply for the issue of a warrant under subsection (2).

(2) On considering an application under subsection (1), a judge of the District Court may issue a warrant authorising the applicant or another authorised officer to enter the premises, but only if the judge is satisfied on the sworn information of the applicant that there are reasonable grounds for suspecting that information required by the applicant or another authorised officer under section 8B is held on any premises.

(3) A warrant issued under subsection (2) authorises the officer named in the warrant, at any time or times within 1 month after the date of issue of the warrant to exercise, by force if necessary, all or any of the powers conferred on authorised officers by section 8B. If, when attempting to enter the premises specified in the warrant, the officer is requested to produce the warrant for inspection, the officer may exercise those powers only after complying with the request.]

Annotations

Amendments:

F34

Inserted (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 35(1) and sch. 1 part 21 item 3, S.I. No. 160 of 2003.

Section 8D

F35[Obstruction of authorised officer when exercising powers.

8D.—A person shall not—

(a) obstruct or interfere with an authorised officer when exercising the powers conferred by this Part, or

(b) without reasonable excuse, fail to comply with a requirement made by an authorised officer under this Part, or

(c) give to an authorised officer information that the person knows or ought to know is false or misleading.]

Annotations

Amendments:

F35

Inserted (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 35(1) and sch. 1 part 21 item 3, S.I. No. 160 of 2003.

Section 8E

F36[Authorised officers may be accompanied by other persons when exercising powers.

8E.—An authorised officer can, if the officer thinks it necessary, be accompanied by a member of the Garda Síochána or by another authorised officer when exercising a power conferred on authorised officers by this Part.]

Annotations

Amendments:

F36

Inserted (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 35(1) and sch. 1 part 21 item 3, S.I. No. 160 of 2003.

Section 8F

F37[Prohibition on unauthorised disclosure of information.

8F.—A person shall not disclose confidential information obtained—

(a) as an authorised officer, or

(b) as a member of the staff of, or as adviser or consultant to, the Director,

unless duly authorised by the Director or by a member of staff authorised by the Director.]

Annotations

Amendments:

F37

Inserted (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 35(1) and sch. 1 part 21 item 3, S.I. No. 160 of 2003.

F38[PART IB

Functions and Powers of Central Bank F39[…] of Ireland]

Annotations

Amendments:

F38

Inserted (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 35(1) and sch. 1 part 21 item 3, S.I. No. 160 of 2003.

F39

Deleted (1.10.2010) by Central Bank Reform Act 2010 (23/2010), s. 15(4) and sch. 2 part 4 item 3, S.I. No. 469 of 2010.

Modifications (not altering text):

C5

Transitional provision prescribed in respect of functions and powers previously vested in Director of Consumer Affairs (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 36 and sch. 3 para. 20(1), S.I. No. 160 of 2003.

Schedule 3 (savings and transitional provisions).

36.—The savings and transitional provisions set out in Schedule 3 have effect.

...

SCHEDULE 3

Savings and Transitional Provisions

...

Performance of former functions of Director of Consumer Affairs

20. (1) If—

(a) before the commencement of section 26 of this Act, action taken by, or done to, the Director of Consumer Affairs in relation to the performance of a function imposed, or the exercise of a power conferred, on the Director by or under a provision of the Consumer Credit Act 1995, and

(b) on that commencement, the function or power became the function or power of the Bank, and

(c) the action had not ceased to have effect before that commencement,

the action continues to have effect as if it had been taken by, or done to, the Bank under that provision as in force after that commencement. Accordingly, if the action relates to the performance of a function, the action must be continued or completed by or in relation to the Bank, and if the action relates to the exercise of a power, the act or thing may be continued or completed by or in relation to the Bank.

Annotations

Amendments:

F40

Inserted (16.05.2022) by Consumer Protection (Regulation of Retail Credit and Credit Servicing Firms) Act 2022(5/2022), s. 14, S.I. No. 229 of 2022.

Section 8G

F40[Interpretation: Part IB.

8G.—(1) In this Part—

"authorised officer" means an authorised officer appointed under section F40[8M];

"designated provisions" means the provisions of this Act referred to in subsection (2);

"Minister" means the Minister for Finance;

F40[…]

(2) The provisions of this Act designated for the purposes of this Part are—

(a) this Part and Parts III, IV, V, VI, VII, VIII, IX and XII, and

(b) Parts II, X and XIII in so far as they apply to persons who enter into agreements with consumers otherwise than as credit intermediaries, and

(c) such other provisions of this Act as are ancillary to those Parts.]

Annotations

Amendments:

Inserted (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 35(1) and sch. 1 part 21 item 3, S.I. No. 160 of 2003.

F41

Substituted (19.12.2012) by Credit Union and Co-operation with Overseas Regulators Act 2012 (40/2012), s. 70 and sch. 4 part 4 item 1(a), S.I. No. 557 of 2012.

F42

Deleted (19.12.2012) by Credit Union and Co-operation with Overseas Regulators Act 2012 (40/2012), s. 70 and sch. 4 part 4 item 1(b), S.I. No. 557 of 2012.

Section 8H

F40[Functions of Bank under this Act.

8H.—(1) The Bank has the following functions for the purposes of this Act:

(a) to keep under general review practices or proposed practices in relation to any of the obligations imposed on persons by or under the designated provisions;

(b) to carry out investigations of any such practices or proposed practices whenever the Bank considers it in the public interest to do so or the Minister so requests;

(c) to request persons engaging in or proposing to engage in such practices as are, or are likely to be, contrary to the obligations imposed on them by a designated provision discontinue or not engage in those practices;

(d) whenever a person in relation to whom such a request has been made engages in or is proposing to engage in any such practice, to bring civil proceedings in the High Court for an order requiring the person to discontinue or not to engage in the practice;

(e) to investigate complaints concerning possible breaches of any of the designated provisions, but at the same time having regard to the availability of other procedures for resolving those complaints;

(f) to publish codes of practice setting out conduct relating to agreements to which the designated provisions apply, in order to secure transparency and fairness in relation to the terms of those agreements and the conduct of agents dealing with consumers under those contracts;

(g) to perform or exercise such other functions as are imposed or conferred on the Bank by this Act.

(2) The Bank may provide in response to complaints or otherwise, information or advice to consumers concerning agreements to which the designated provisions apply, and, in particular, on the obligations imposed on creditors or other persons by those provisions.]

Annotations

Amendments:

F43

Inserted (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 35(1) and sch. 1 part 21 item 3, S.I. No. 160 of 2003.

Section 8I

F40[Bank to provide information to Minister.

8I.—The Bank shall provide the Minister with such information regarding the performance or exercise of the Bank's functions under this Act as the Minister may require from time to time.]

Annotations

Amendments:

F44

Inserted (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 35(1) and sch. 1 part 21 item 3, S.I. No. 160 of 2003.

Section 8J

F40[Bank to prepare annual report of its activities under this Act.

8J.—(1) The Bank shall, within 4 months after the end of each financial year, prepare a report setting out the Bank's activities in that year in relation to the performance or exercise of the Bank's functions under this Act.

(2) The Bank shall include the report in, or attach the report to, the report presented to the Minister under section 61 of the Central Bank Act 1942.]

Annotations

Amendments:

F45

Inserted (1.5.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 35(1) and sch. 1 part 21 item 3, S.I. No. 160 of 2003.

Section 8K

F40[Powers of Bank in respect of investigations.

8K.—(1) In conducting an investigation under the designated provisions, the Bank may—

(a) require any person who, in the opinion of the Bank is in possession of information, or has or has access to a record or thing, that is relevant to the investigation to provide the information, record or thing to the Bank, and

(b) where appropriate, require the person to attend before the Bank for that purpose.

(2) A person to whom a requirement is made under this section shall comply with the requirement, but in doing so is entitled to the same immunities and privileges as if the person were a witness before a court.

(3) A person shall not obstruct or interfere with the Bank in the performance or exercise of the Bank's functions under this Act.]

Annotations

Amendments:

F46

Inserted (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 35(1) and sch. 1 part 21 item 3, S.I. No. 160 of 2003.

Section 8L

F40[Directions of Bank in respect of statements and notices.

8L.—(1) The Bank may, in the interests of better informing consumers, give directions as to the location and size of any statement or notice required under the designated provisions. The directions may be given in such manner as the Bank thinks fit.

(2) A person to whom such a direction is given shall comply with the direction.]

Annotations

Amendments:

F47

Inserted (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 35(1) and sch. 1 part 21 item 3, S.I. No. 160 of 2003.

Section 8M

F40[Appointment of authorised officers for purposes of this Part.

8M.—(1) F40[The Minister] may in writing appoint persons to be authorised officers for the purposes of all or any of the designated provisions.

(2) An appointment under this section may be for a specified or unspecified period.

(3) F40[The Minister] who appoints an authorised officer shall provide the officer with a certificate of authority.

(4) Whenever an authorised officer is requested to do so by a person in relation to whom the officer is exercising a power under the designated provisions, the officer shall produce the officer's certificate of authority together with some form of personal identification.

(5) The appointment of a person as an authorised officer ends—

(a) when F40[the Minister] concerned revokes the appointment or the person dies or resigns from the appointment, or

(b) if the appointment is for a fixed period, when the period ends, or

(c) if the person appointed is an officer of F40[the Minister], when the person ceases to be such an officer.]

Annotations

Amendments:

F48

Inserted (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 35(1) and sch. 1 part 21 item 3, S.I. No. 160 of 2003, subject to transitional provision in s. 36 and sch. 3 para. 22.

F49

Substituted (19.12.2012) by Credit Union and Co-operation with Overseas Regulators Act 2012 (40/2012), s. 70 and sch. 4 part 4 item 2, S.I. No. 557 of 2012.

Editorial Notes:

E38

Previous affecting provision: persons authorised under section deemed to be authorised (2.07.2002) for purposes of European Communities (Cross Border Payments in Euro) Regulations 2002 (S.I. No. 335 of 2002), reg. 3(2), as amended (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 35(2) and sch. 2 part 19 item 2, S.I. No. 160 of 2003; revoked (19.05.2010) by European Communities (Cross Border Payments) Regulations 2010 (S.I. No. 183 of 2010), reg. 21, in effect as per reg. 1(2).

Section 8N

F40[Powers of authorised officers.

8N.—(1) An authorised officer may, for the purpose of carrying out an investigation under this Part, do all or any of the following:

(a) at all reasonable times enter any premises, at which there are reasonable grounds to believe that—

(i) a trade or business, or any activity relating to a trade or business, is, or has been, carried on, or

(ii) records relating to a trade, business or activity are kept;

(b) search and inspect premises entered under paragraph (a) and any records on the premises;

(c) secure the premises or part of the premises for later inspection, or any part of the premises in which the officer reasonably believes records relating to a trade or business are kept;

(d) require any person who carries on a trade, business or activity, or any person employed in or in connection with it—

(i) to produce to the officer records relating to the trade, business or activity, and

(ii) if the information is in a non-legible form, to reproduce it in a legible form or to give to the officer such information as the officer reasonably requires in relation to entries in the records;

(e) inspect and take copies of records inspected or produced under this section (including in the case of information in a non-legible form, a copy of all or part of the information in a permanent legible form);

(f) remove and retain the records inspected or produced under this section for such period as may be reasonable to facilitate further examination (subject to the issue of a warrant for that purpose by a judge of the District Court);

(g) require any such person to give to the officer information that the officer reasonably requires in relation to the trade, business or activity concerned, or in relation to the persons carrying on that trade, business or activity or employed in or in connection with it;

(h) require any such person to give to the officer any other information which the officer may reasonably require in regard to the trade, business or activity concerned;

(i) require any person by whom or on whose behalf data equipment is or has been used, or any person who has charge of, or is otherwise concerned with the operation of, the equipment or any associated apparatus or material, to give the officer all reasonable assistance in relation to the equipment, apparatus or material;

(j) require any other person employed in or in connection with the trade, business or activity concerned to give to the officer, at any reasonable time, information that the officer reasonably requires in relation to that trade, business or activity and to produce to the officer any records that the person has or has access to.

(2) An authorised officer shall not, except with the consent of the occupier, enter a private dwelling unless the officer has obtained a warrant from the District Court under section 8N authorising the entry.]

Annotations

Amendments:

F50

Inserted (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 35(1) and sch. 1 part 21 item 3, S.I. No. 160 of 2003.

Section 8O

F40[Issue of search warrants.

8O.—(1) If an authorised officer is prevented from entering premises under section 8N, the officer or another authorised officer may apply for the issue of a warrant under subsection (2).

(2) On considering an application under subsection (1), a judge of the District Court may issue a warrant authorising the applicant or another authorised officer to enter the premises, but only if the judge is satisfied on the sworn information of the applicant that there are reasonable grounds for suspecting that information required by the applicant or another authorised officer under section 8N is held on any premises.

(3) A warrant issued under subsection (2) authorises the officer named in the warrant, at any time or times within 1 month after the date of issue of the warrant to exercise, by force if necessary, all or any of the powers conferred on authorised officers by section 8N. If, when attempting to enter the premises specified in the warrant, the officer is requested to produce the warrant for inspection, the officer may exercise those powers only after complying with the request.]

Annotations

Amendments:

F51

Inserted (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 35(1) and sch. 1 part 21 item 3, S.I. No. 160 of 2003.

Section 8P

F40[Obstruction of authorised officer when exercising powers.

8P.—A person shall not—

(a) obstruct or interfere with an authorised officer when exercising the powers conferred by this Part, or

(b) without reasonably excuse, fail to comply with a requirement made by an authorised officer under this Part, or

(c) give to an authorised officer information that the person knows or ought to know is false or misleading.]

Annotations

Amendments:

F52

Inserted (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 35(1) and sch. 1 part 21 item 3, S.I. No. 160 of 2003.

Section 8Q

F40[Authorised officers may be accompanied by other persons when exercising powers.

8Q.—An authorised officer can, if the officer thinks it necessary, be accompanied by a member of the Garda Síochána or by another authorised officer when exercising a power conferred on authorised officers by this Part.]

Annotations

Amendments:

F53

Inserted (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 35(1) and sch. 1 part 21 item 3, S.I. No. 160 of 2003.

F54[PART IC

Provisions Applicable to Director and Bank]

Annotations

Amendments:

F54

Inserted (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 35(1) and sch. 1 part 21 item 4, S.I. No. 160 of 2003.

Section 9

APR.

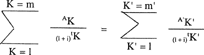

9.—(1) In this Act the APR shall be the equivalent, on an annual basis, of the present value of all commitments (loans, repayments and charges), future or existing, F55[agreed, in the case of a credit agreement, by the creditor and the consumer and, in the case of a hire-purchase agreement, by the owner and the hirer], calculated to the nearest rounded decimal place in accordance with the method of calculation specified in the Fourth Schedule.

(2) The F56[Bank] may by regulations amend the method of calculation of the APR specified in the Fourth Schedule either generally F57[or in relation to any form of credit covered in this Act or in relation to hire-purchase agreements].

(3) The F56[Bank] shall, from time to time, publish guidelines to explain the method of calculation of the APR under this Act.

Annotations

Amendments:

F55

Substituted (16.05.2022) by Consumer Protection (Regulation of Retail Credit and Credit Servicing Firms) Act 2022 (5/2022), s. 12(a), S.I. No. 229 of 2022.

F56

Substituted (1.05.2003) by Central Bank and Financial Services Authority of Ireland Act 2003 (12/2003), s. 35(1) and sch. 1 part 21 item 5, S.I. No. 160 of 2003, subject to transitional provision in s. 36 and sch. 3 para. 20(1).

F57

Substituted (16.05.2022) by Consumer Protection (Regulation of Retail Credit and Credit Servicing Firms) Act 2022 (5/2022), s. 12(b), S.I. No. 229 of 2022.

Section 10

Criteria for calculation of APR.

10.—(1) This section shall apply to credit agreements other than housing loans.

(2) For the purpose of calculating the APR the total cost of credit to the consumer shall be determined, with the exception of the following charges:

(a) charges payable by the consumer for non-compliance with any of his commitments laid down in the credit agreement,

(b) charges other than the purchase price which, in purchases of goods or services, the consumer is obliged to pay whether the transaction is paid in cash or by credit,

(c) charges for the transfer of funds and charges for keeping an account intended to receive payments towards the reimbursement of the credit, the payment of interest and other charges except where the consumer does not have reasonable freedom of choice in the matter and where such charges are abnormally high; this paragraph shall not, however, apply to charges for collection of such reimbursements or payments, whether made in cash or otherwise,

(d) membership subscriptions to associations or groups and arising from agreements separate from the credit agreement, even though such subscriptions have an effect on the credit terms,

(e) charges for insurance or guarantees other than those designed to ensure payment to the creditor, in the event of the death, invalidity, illness or unemployment of the consumer, of a sum equal to or less than the total amount of the credit together with relevant interest, and other charges imposed by the creditor as a condition for credit being granted.

(3) (a) The APR shall be calculated—

(i) in the case of a credit agreement, at the time the agreement is concluded, or

(ii) in the case of an advertisement which relates to the offering of credit and mentions the APR, at the time the advertisement is published, and

(b) the calculation shall be made on the assumption that the credit agreement is valid for the period agreed and that the creditor and the consumer fulfil their obligations under the terms and by the dates agreed.

(4) In the case of credit agreements containing terms allowing variations in the rate of interest and the amount or level of other charges contained in the APR but unquantifiable at the time when it is calculated, the APR shall be calculated on the assumption that interest and other charges remain fixed and will apply until the end of the credit agreement. The variability shall be indicated with equal prominence to and along with the APR.

(5) In the case of credit agreements containing terms allowing variations in the rate of interest and the amount or level of other charges contained in the APR but quantifiable at the time when it is calculated, the APR shall be calculated to take account of the rates applicable from the specific dates set out in the agreement.

(6) Where necessary, the following assumptions may be made in calculating the APR:

(a) if there is no fixed timetable for repayment, and one cannot be deduced from the terms of the credit agreement and the means for repaying the credit granted, the duration of the credit shall be deemed to be one year,

(b) unless otherwise specified, where the credit agreement provides for more than one repayment date, the credit will be made available and the repayments made at the earliest time provided for in the agreement,

(c) where the amount of credit to be provided is not specified—

(i) in the case of running account credit, where a credit limit is specified, it shall be assumed that the maximum amount of credit is provided for the duration of the agreement, and

(ii) in any other case, it shall be assumed that the amount provided shall be £1,000,

(d) where charges are payable at an unspecified date after the agreement is signed it shall be assumed that they are payable at the beginning of the agreement.

(7) A creditor shall comply with the requirements of this section in relation to the calculation of the APR in respect of a credit agreement.

Section 11

Laying of regulations before Houses of Oireachtas.

11.—Every regulation made under this Act shall be laid before each House of the Oireachtas as soon as may be after it is made and, if a resolution annulling the regulation is passed by either such House within the next 21 days on which that House has sat after the regulation is laid before it, the regulation shall be annulled accordingly but without prejudice to the validity of anything previously done thereunder.

Section 12

Offences.

12.—F58[(1) A person commits a summary offence under this Act if the person—

(a) in Part IA, contravenes section 7(2) or (3), 8(2), 8D or 8F, or

(b) in Part IB, contravenes section 8K(2) or (3), 8L(2) or 8P, or

(c) in Part II, contravenes section 26 or 27, or regulations under section 28, or

F59[(ca) in Part IIA, contravenes section 28A(2) or 28B(2), or]

(d) in Part III, contravenes section 39, or

(e) in Part IV, contravenes section 43(2), or

(f) in Part VI, contravenes section 61, 64 (1) or 69, or

(g) in Part VII, contravenes section 87 or 91, or

(h) in Part VIII, contravenes section 93(6) or (9), 94, 95, 98(4) or (5), 99, 105(3) or (4), 106(2) or (3), or

(i) in Part IX, contravenes section 116(1) or (2), 117, 122(3), 123, 124, 128, 129(2), 130, 131(4) or (5), 132, 133(1) or (2), 134 or 135(3), or

(j) in Part X, contravenes section 138, 139, 142 or 143(2), or regulations made under section 137, or

(k) in Part XI, contravenes section 144(1) or (3), 145 or 148.

(2) A person commits an offence under this Act (other than a summary offence) if the person—

(a) in Part IV, contravenes section 45, 46 or 49, or

(b) in Part V, contravenes section 54, or

F60[(c) in Part VIII, contravenes section 94A(1), 96, 97, 98(1) or (2), 98A(1), 100, 101, 102, 103(2), 107, 110 or 111, or]

(d) in Part IX, contravenes section 118 or 127, or

(e) in Part X, contravenes section 140, or